PM9 - Research Paper. Rozen-Bakher, Z. The Impact of Mergers and Acquisitions Strategy on Labour Productivity: The Mediation Role of the Integration

Rozen-Bakher, Z. The Impact of Mergers and Acquisitions Strategy on Labour Productivity: The Mediation Role of the Integration. Research Paper, PM9. https://www.rozen-bakher.com/research-papers/pm9

COPYRIGHT ©2019-2024 ZIVA ROZEN-BAKHER ALL RIGHTS RESERVED

Rozen-Bakher, Z.

The Impact of M&A Strategy on Labour Productivity: The Mediation Role of the Integration

Abstract

This study raises the question of whether the M&A strategy leads to the creation of special conditions in relation to labour productivity due to the integration. Under normal conditions, if a firm produces more output with the same inputs or produces the same output at a lower cost, then it’s supposed to lead to an improvement in labour productivity, while under conditions of M&As, if a firm reduces its number of workers during the integration stage to remove redundancies, then it may hinder the ability to realize the synergy potential because of the shortage of employees, which may negatively influence the labour productivity. The results show that seizing synergy leads to an increase in the output of the M&A, while the reduction of workforce size leads to a decrease in the input of the M&A, still, the study reveals that the M&A strategy leads to a positive effect on labour productivity if the integration process was ended in success. However, the study indicates that an increase in the workforce size helps to successfully end the integration stage because there is no shortage in human resources to realize synergy potential, but at the same time, it hinders the ability to improve labour productivity. This may explain the high failure rate of M&A strategy because it shows the challenges in achieving both synergy success and an improvement in labour productivity.

Keywords: Integration, Labour Productivity, Mergers and Acquisitions (M&A), Performances

Introduction

Due to the high failure rate of the M&A strategy (Alkaraan, 2019; Angwin & Savill, 1997; Jap et al., 2017; King et al., 2004; Kumar & Sharma, 2019; Puranam et al., 2006; Renneboog & Vansteenkiste, 2019; Rozen-Bakher, 2018c, 2018d: Sarala, 2010; Steger & Kummer, 2007; Thelisson, 2020; Tichy, 2001; Venema, 2015; Wangerin, 2019; Weber et al., 2012), this study raises the question if the implementation of M&A strategy can result in the creation of special conditions in relation to labour productivity because of the integration process. Labour productivity is considered a crucial organizational outcome (Datta et al., 2005). Scholars have defined labour productivity as the total output divided by labour inputs (Samuelson & Nordhaus, 1989), which indicates the efficiency of the labour force in creating the output of the firm (Datta et al., 2005). Thus, an improvement in labour productivity reflects the relative contribution of every worker in the achievement of the overall income of the firm (Datta et al., 2005; Huselid, 1995; Guthrie, 2001; Koch & McGrath, 1996). Therefore, labour productivity could provide a measure of the firm success (Dyer & Reeves, 1995).

In the light of the above, under normal conditions, if a firm produces more output with the same inputs or produces the same output at a lower cost, then it’s supposed to lead to an improvement in labour productivity. However, under conditions of implementation of M&A strategy, if a firm reduces its number of workers during the integration stage with the aim of eliminating duplicate jobs, overlapping activities (Lehto & Böckerman, 2008) and consolidation of functions to remove redundancies (Krishnan & Park, 2002), then it may hinder the ability to realize the synergy potential because of the shortage of employees, and as a result, it may negatively influence the labour productivity.

Considering these arguments outlined above, this study raises several important research questions, as follows:

(i) Do M&As lead to improvement in labour productivity?

(ii) Does the implementation of an M&A strategy create special conditions in relation to labour productivity due to the integration process?

(iii) Are there differences between the integration success and the integration failure in relation to the labour productivity in M&As?

(iv) Does the integration process mediate the relationship between the output (synergy success) and the input (workforce change during the integration process) of the M&A and the labour productivity in the post-M&A period?

The existing literature lacks studies that examine the impact of the implementation of the M&A strategy on labour productivity, particularly during the integration stage. The study of Conyon et al. (2002) examines the influence of foreign acquisition on labour productivity, yet this study focuses on the acquisition of on-going firms by foreign and domestic firms in the UK manufacturing industry for the period 1989-94 (Conyon et al., 2002), rather than on the influence of the integration process on the labour productivity. Besides, the M&A literature lacks studies that examine the integration process as a mediator variable in relation to labour productivity. Moreover, and even more importantly, the M&A literature has not developed theoretical background, if the implementation of M&A strategy can lead to the creation of special conditions in relation to labour productivity due to the integration process. This understanding may help to identify the reasons for the high failure rate of M&A strategy with the aim of lowering the risks involves in M&A activity. At the methodological level, there are existing studies that examine the influence of M&A activity in relation to productivity (e.g. Ferrier & Valdmanis, 2004; Harris & Robinson, 2002; Karpaty, 2007; Lichtenberg et al., 1987), but these studies used the measure of total factor productivity (TFP) rather than the labour productivity. The TFP is based on the inputs of the labour and the capital (Gordon, 2016), while the labour productivity is based only on the input of the labour (Conyon et al., 2002). In other words, the TFP refers to the measure of output per worker and capital inputs, while labour productivity refers to the measure of output per worker. Bryan (2007) argues that in the digital age, the performances need to focus on the return on talent rather than on the return on capital because intangible assets are a rich source of value like talent workers. Therefore, the managers should increase the profit relative to the number of people a company employs, but at the same time, the firm needs to shed the low-profit employees with the aim of improving the profit per employee (Bryan, 2007). This argument highlights the importance of understanding how the M&A activity influence labour productivity (only labour) rather than the TFP (labour and capital) because of the nature of the integration process that is supposed to lead to workforce reduction, and as a result, it is expected to influence the labour productivity. This exploration of labour productivity in M&As is highly important because of the problematic integration process that may explain the high failure rate of M&A strategy, regardless of the importance of using the TFP in other studies. Furthermore, the accelerating of employment shifts in the last decades from the industry sector to the services sector (Rozen-Bakher, 2017; Schettkat & Yocarini, 2006), leads to an increase in production output per worker due to the economic development that affects the efficiency (Clark, 1940). This trend is supposed to lead to more influence on labour productivity in the industry sector compared to the services sector because of the decline in the ratio of employees engaged in production in the industry sector (Clark, 1940). There are studies in the literature that examine the labour productivity in specific sub-sectors of the industry sector, such as the construction sector (Enshassi et al., 2007), the electronics Industry (Liu, 2001), and the manufacturing sector (Aggrey et al., 2010; Cobet & Wilson, 2002; Mahmood, 2008; Lichtenberg et al., 1987). However, the existing literature lacks studies that examine the labour productivity in the whole industry sector nor the labour productivity in M&As of the industry sector.

In the light of the above, this study seeks to fill some of these research gaps. Therefore, the goal of the present study is to explore if the implementation of an M&A strategy can result in the creation of special conditions in relation to labour productivity due to the integration process. This may contribute to the understanding of how M&A strategy affects labour productivity and may also help for explaining the high failure rate of M&A strategy. To address this goal, this study presents a mediation model with the aim of examining if the integration process mediates the relationship between the output (synergy success) and the input (workforce change during the integration process) of the M&A and the labour productivity in the post-M&A period. The study focuses on the industry sector because this sector is more likely to be affected by the integration process due to the labour-intensive firms that characterize this sector.

The study is organised as follows: The next section outlines the theoretical background and hypotheses. The following sections describe the methodology and present and discuss the results. The final sections present the conclusions, discuss the limitations of the study, and give recommendations for future studies.

Theoretical Background and Hypotheses

Figure 1 presents the research model that guides this study with the aim of exploring if the implementation of an M&A strategy creates special conditions in relation to labour productivity due to the integration process, as discussed in the following section. The research model includes the three stages of the M&A process − the pre-M&A stage, the integration stage and the post-M&A stage (Caiazza & Volpe, 2015) − to explore the change in labour productivity during the M&A process.

Labour Productivity Under Implementation of M&A strategy

Labour productivity has been identified as a crucial indicator for workforce performance (Delery & Shaw, 2001) and it also offers an indication of the success of the firm (Dyer & Reeves, 1995). However, despite that labour productivity is considered an important organizational outcome (Datta et al., 2005), the M&A literature neglects this topic. The M&A literature lacks both theoretical studies and empirical studies in relation to labour productivity. The M&A literature doesn’t provide theoretical background if there is a difference between labour productivity under conditions of implementation of M&A strategy and under normal conditions when the firm doesn’t involve in M&A activity. This lack in the M&A literature limits the ability to develop well-grounded assumptions based on the existing studies. Despite this limitation, this study developed assumptions based on a synthesis of two bodies of literature. The first one deals with productivity in general and with labour productivity in particular. The second one deals with M&A activity, especially with the integration process. Hence, this study may consider as pioneering research in relation to labour productivity in M&As.

Based on the synthesis of these two bodies of literature, this study assumes that there is a difference between firms that operate under normal conditions and under the implementation of M&A strategy in relation to the change in labour productivity, as shown in figure 2 that presents the differences in labour productivity under normal conditions and under M&A strategy. As shown in figure 2, there are several possibilities for improvement in labour productivity under normal conditions. If a firm reduces its number of workers, with achieving the volume of activity mark or sees even an increase in it, then it can lead to improvement in labour productivity. This can occur in cases of reduction of the excess workforce, which is not harming the functioning of the firm and the business results. However, if a firm increases the volume of activity without changing the workforce size or even reducing it, then it can lead to improvement in labour productivity. Nevertheless, in a situation of a decline in the business results because of external factors, such as in case of economic crisis, then the labour productivity may be harmed. This can be prevented if the firm adjusts its business results through an increase of efficiency and reduction of workforce.

Theoretically, an M&A strategy is also supposed to lead to improvement in labour productivity due to the combination of seizing synergies along with the reduction of workforce size during the integration stage. Seizing synergy potential in M&As is the first key to improving labour productivity because it’s supposed to lead to an increase in the volume of the activity of the combined firm. Synergy refers to the ability of the combined firm to generate greater value after the M&A compared to their ability to generate value before the M&A took place when each firm was working apart (Calipha et al., 2010; O'Shaughnessy & Flanagan, 1998). Carpenter and Sanders (2007) argue that there are five motives for generating synergy success: reducing threats, increased market power, cost savings, increased financial strength and leveraging capabilities. Porter (1985) argues that the main objective of an M&A is to improve the competitive advantage of the firms. However, Larsson and Finkelstein (1999) argue that synergy can be achieved through ‘economies of sameness’ that could arise from the expansion of similar operations and technologies, or through ‘economies of fitness’ that could arise from different products, markets and knowledge. Seth (1990) puts emphasis on the production synergies, which exist when the cost of the joint production of two goods after the M&A is less than the costs of production of these goods by the two single-product firms before the M&A. Synergies could also be achieved through purchasing or inventory management in cases that the combined firm using common raw materials or components. Besides production, sharing areas of a business, such as advertising, distribution, services, and R&D (Porter, 1980) could also lead to synergies (Seth, 1990). Other scholars argue that synergy could be achieved through the transfer of capabilities and resource sharing (Graebner, 2004; Weber et al., 2011) whether they are tangible or intangible, such as sharing information (Shaver, 2006) or knowledge, resulting in an increase in the volume of activity of the M&A (Graebner, 2004; Weber et al., 2011). In the light of the above, synergies are serving as sources for increasing the output of the combined firm, which is supposed to lead to an improvement in labour productivity. In the light of the arguments presented above, here is the first hypothesis:

· Hypothesis 1: Synergy success in M&As has a positive effect on labour productivity in the post-M&A stage.

Workforce reduction during the integration process in M&As is the second key to improving labour productivity. The workforce reduction is defined as an activity that is undertaken by the management of an organization to improve efficiency, productivity, and competitiveness (Freeman & Cameron, 1993). The integration process in M&A activity should lead to workforce reduction (Deakin & Slinger, 1997; Gibbs, 1993; Haspeslagh & Jemison, 1991; Lehto & Böckerman, 2008; O’Shaughnessy & Flanagan, 1998). The integration process refers to changes in the functional activities, structures and cultures of the organizations with the aim of simplifying the consolidation of the two firms into a functioning whole (Pablo, 1994; Stahl & Voigt, 2008). The resource-based perspective argues that workforce reduction will result in operational synergies during the process of integrating the target firm into the acquirer’s organization (Lubatkin, 1983). The existing studies support the argument that M&As lead to workforce reduction (Deakin & Slinger, 1997; Lehto & Böckerman, 2008), particularly during the integration stage (Haspeslagh & Jemison, 1991) due to the elimination of duplicate jobs, overlapping activities (Lehto & Böckerman, 2008) and consolidation of functions to remove redundancies (Krishnan & Park, 2002). In some M&As, the acquirer even decided to close the target’s corporate headquarter (Krishnan & Park, 2002), resulting in the elimination of the target’s workforce. This happens particularly when implemented exit strategy (Rozen-Bakher, 2017), which often leads to a reduction in jobs (Kane, 2010). However, Cappelli (2000) distinguishes between downsizing that is undertaken to improve efficiency, which is driven by internal factors, and layoffs that are undertaken to respond to external factors, such as shortfalls in the product demand. John et al. (2015) also argue that in the case of an unprofitable firm, the organization is more likely to lay off employees. Therefore, acquiring an inefficient target is supposed to lead to cost-cutting (Rhoades, 1998) and workforce reduction (Vennet, 1996), particularly in labour-intense target firms (Froud et al., 2000). An M&A also creates an opportunity to gain short-term profit if the acquirer reduces the workforce size by not abiding by the employees’ contracts made by the management of the target before the M&A took place (Kubo & Saito, 2012). Moreover, the existing studies show differences between firms from the industry sector and the other sectors. Lehto and Böckerman (2008) show that M&As lead to downsizing in manufacturing firms, while the effect on employment in non-manufacturing firms are much weaker. However, McGuckin and Nguyen (2001) show that ownership change in manufacturing is associated with job loss, but only in relation to larger plants. Considering the above, if an M&A allows the firm to produce the same output or even more output at a lower cost (Tremblay & Tremblay, 2012), the workforce reduction during the integration process is supposed to lead to an improvement in labour productivity. Considering the arguments outlined above, here is an additional hypothesis:

Hypothesis 2: Workforce reduction during the integration stage has a positive effect on labour productivity in the post-M&A stage.

The Mediating Role of the Integration Process: Integration Success Versus Integration Failure

The existing literature lacks studies that exploring of whether the integration process mediates the relationship between the output (synergy success) and the input (workforce change) of the M&A and the labour productivity in the post-M&A stage. Despite this limitation, this study developed assumptions based on the integration literature. Based on this literature, the present study assumes that the success or the failure of the integration process may lead to a different impact on labour productivity, as shown in figure 2. Even more importantly, this study assumes that the implementation of an M&A strategy can create special conditions in relation to labour productivity, particularly in cases when the integration process is implemented in ineffective ways, which may result in a decline in labour productivity.

The integration process is considered the ‘weakest link’ of M&A strategy (Rozen-Bakher, 2018d). The integration process is supposed to create a ‘bridge’ between the pre-M&A stage and the post-M&A stage. The main objective of the integration process is to seize the synergy potential (Graebner, 2004; Weber et al., 2011) by integrating the two firms into one firm that combines the functions of the acquirer and the target. The nature of this process includes the elimination of duplicate jobs, activities, and functions to remove redundancies (Krishnan & Park, 2002; Lehto & Böckerman, 2008) with the objective of improving efficiency through cost-cutting (Rhoades, 1998), which is supposed to lead to downsizing of the workforce (Deakin & Slinger, 1997; Gibbs, 1993; Haspeslagh & Jemison, 1991; Lehto & Böckerman, 2008; O’Shaughnessy & Flanagan, 1998). Therefore, if the integration process is implemented in effective ways, then it may produce positive performances (Larsson & Finkelstein, 1999; Weber et al., 2011; Zollo & Meier, 2008), resulting in an improvement in labour productivity. For this reason, the integration success is a vital element for achieving M&A success (e.g., Jemison & Sitkin, 1986; Mitchell & Shaver, 2003; Pablo, 1994; Shaver, 2006; Zollo & Singh, 2004) and as a result, it's supposed to lead to an improvement in labour productivity. In sum, integration success allows achieving both synergy success and workforce reduction, resulting in an improvement in labour productivity. In the light of the arguments presented above, here are two hypotheses:

· Hypothesis 3: Integration success has a positive effect on labour productivity in the post-M&A stage.

· Hypothesis 4: Integration success mediates the relationship between the output (synergy success) and the input (workforce change during the integration process) of the M&A and the labour productivity in the post-M&A stage.

The integration success is supposed to lead to an improvement in labour productivity. However, Shaver (2006) argues that it is possible to merge previously two independent firms yet fail to integrate them. Many existing studies confirm this argument, that in many M&As, the integration stage was ended in a problematic process that negatively influence the success of the M&A (Baunsgaard & Clegg, 2013; Chen & Wang, 2014; Mtar, 2010; Shimizu et al., 2004; Very et al., 1996; Yu et al., 2005). For that reason, M&A strategy has a high risk for failure (Chen & Wang, 2014) due to the problematic integration stage (Baunsgaard & Clegg, 2013; Kroon et al., 2015; Krug & Nigh, 2001; Mtar, 2010; Shimizu et al., 2004; Very et al., 1996; Weber et al., 2011, 2012; Yu et al., 2005). The main explanation for the failure of the integration stage lays in the mismatch between the acquirer and the target that lead to obstacles during the integration process, which hinder the ability to achieve the objectives of the M&A strategy. In the integration stage, the two firms must learn to work together with the aim of realizing synergy potential. However, if the integration process is not effective, it can lead to negative implications, such as a culture clash (Weber et al., 2011), political infighting within the organization (Calandro, 2008) and resistance to integration-related change (Schweizer, 2005; Piske, 2002). This could even lead to the turnover of top management (Ahammad et al., 2012; Lubatkin et al., 1999), resulting in a serious loss of valuable resources (Weber et al., 2011). Besides, if the integration process creates uncertainty and confusion within the organization (Jemison & Sitkin, 1986), it can unintentionally prompt a large-scale workforce reduction (Krishnan & Park, 2002; Lehto & Böckerman, 2008). In other words, the downsizing is supposed to be accordingly to the planning of the integration process rather than unintentional downsizing. In unintentional downsizing, many employees often decided to leave voluntarily the organization during the integration stage because of their unwillingness to deal with the negative implications of the M&A, resulting in a shortage of human resources. Voluntary turnover is negatively related to labour productivity because it reduces the stock of firm-specific human capital that a firm retains. (Yanadori & Kato, 2007). Voluntary turnover is more likely to be among key workers that have more job opportunities in other organizations, which negatively influence the knowledge of the organization, particularly in cases that many key workers leave the organization simultaneously. The knowledge of the workers is necessary to seize synergies (Hitt et al., 2001). Therefore, loss of such knowledge could hinder the ability to realize synergy potential (Krishnan et al., 2007), resulting in a negative effect on the outcome of the combined firm. Moreover, large-scale downsizing can harm the motivation of the workers, which may lead to a lower degree of willingness of the surviving employees to invest effort in their jobs, such as satisfying the customers (Krishnan et al., 2007). Therefore, limited capacity increases the possibility that the combined firm will not be able to realize fortuitous outcomes from the merged businesses because of the capacity constraints (Shaver, 2006). Labour productivity can also be negatively affected by the downsizing (Guthrie, 2001), particularly in cases in which the employee’s morale and welfare are harmed (Iverson & Zatzick, 2011). These outcomes negatively influence the business performances of the M&A (Hambrick & Cannella, 1993) and as a result, it leads to a decline in labour productivity. In sum, the implementation of an M&A strategy can create special conditions in relation to labour productivity due to the integration process. The nature of the integration process is supposed to lead to workforce reduction, but if the integration process is implemented ineffectively, it may hinder the ability to realize the synergy potential, which results in a decline in labour productivity. In the light of the arguments presented above, the following two hypotheses are proposed:

· Hypothesis 5: Integration failure in M&As has a negative effect on labour productivity in the post-M&A stage.

· Hypothesis 6: Integration failure mediates the relationship between the output (synergy success) and the input (workforce change during the integration process) of the M&A and the labour productivity in the post-M&A stage.

Methodology

Sample and Data Sources

The sample of the study included 198 public firms (99 acquirers and 99 targets) from the industry sector that were involved in M&A activity. These public firms have traded on the stock exchange of the NASDAQ Stock Market (NASDAQ, 2021) and the New York Stock Exchange (NYSE) (NYSE, 2021). The classification of the industry sector in this study is based on the International Standard Industrial Classification (ISIC) of the United Nations industry classification system. Therefore, the industry sector of this study includes the categories C–F of the ISIC, as follows: mining and quarrying, manufacturing, electricity, gas and water supply, and construction. The industry sector of the sample is based on the sector of the target before the M&A took place. In addition, the public firms included in the sample are from 10 countries, as follows: Australia, Bermuda, Canada, Cayman Islands, Chile, France, Germany, Switzerland, United Kingdom and the United States. Besides, the study sample includes only a single M&A (Lubatkin, 1987) rather than a multiple M&A that was carried out by the acquirer during the year that the M&A took place (Krishnan et al., 2007; Krishnan & Park, 2002). Measuring multiple M&A can create ‘noises’ due to additional factors that may influence the analysis of M&A success. This may happen in cases that the acquirer buys additional targets during the research period.

Moreover, the study database was based on 396 annual reports (10-K) of the public firms included in the sample. These annual reports are required by the U.S. Securities and Exchange Commission (SEC) and are considered a reliable source about the performances of the firms (SEC, 2021; Rozen-Bakher, 2018b). Importantly, accordingly, to the SEC, all the public firms that have traded on the stock exchanges in the USA, must publish the annual reports (10-K) (Rozen-Bakher, 2018c; SEC, 2021), so the public has free access to these annual reports (Rozen-Bakher, 2018c). Hence, these reports allow comparison among many firms because the SEC requests the same financial measures from all the public firms.

Research Method

Evaluation Method. There are three main methods for evaluation of micro-performance in M&A studies (Rozen-Bakher, 2018a, 2018c), as follows:

(i) The event study method. This method considers an M&A as a single event and the date of the merger announcement determines as the centre of the “event period” (Changjun & Qiaoyue, 2014). Accordingly, these studies examine the influence of the merger announcement on the price fluctuations of the stock market (Changjun & Qiaoyue, 2014). However, there is a criticism in the existing literature regarding this method when it used in studies that examine long post-M&A success. Oler et al. (2008) found that the positive initial market response to an acquisition announcement is contradicted by negative long-run post-M&A returns, so they conclude that a short-window analysis may not fits for examining long post-M&A success.

(ii) The respondents’ self-estimated rating method. This method assesses M&A success through managers’ questionnaires (Ahammad et al., 2012; Angwin & Savill, 1997; Pablo, 1994; Piske, 2002). This method relies on the perception of the managers (Weber et al., 2011), which may be biased for reasons like managers’ need to report successful achievement or lack of information of the managers (Huber & Power, 1985). In addition, there is a limitation to comparing the performances between the pre-M&A stage and the post-M&A stage (Weber et al., 1996) based on this method, because the managers will not necessarily retain their positions during the research period.

(iii) Accounting Research Method. This method focuses on the financial statements and accounting data with the aim of comparing the changes in the financial performances between the pre-M&A period and the post-M&A period (Rozen-Bakher, 2018a, 2018b), such as changes in profitability (Ramaswamy, 1997) sales (Changjun & Qiaoyue, 2014) and more. However, this method has a limitation in exploring quality performances and strategic performances (Chakravarthy, 1986). Therefore, the accounting method is preferable for quantity performances because it shows more the actual performances compared to the other methods (Rozen-Bakher, 2018a). In addition, the accounting research method is preferable for comparing the changes in performances during the M&A process (Rozen-Bakher, 2018c), because the event study method focuses on the present value of future streams of income, whereas the accounting research method focuses on past performances (Seth, 1990), which allow exploring the real outcomes of the M&A in the post-M&A period. Given these considerations, the present study is based on the accounting research method. Accordingly, the analysis of the study is based on the annual reports (10-K) of the public firms included in the sample.

Time Series Analysis. This study includes the three stages of the M&A process: pre-M&A stage, integration stage and post-M&A stage (Caiazza & Volpe, 2015; Rozen-Bakher, 2018a, 2018c), as follows:

(i) Pre-M&A Stage. This stage refers to the pre-M&A period. The data of this stage are based on the sum of the performances of the acquirer and target before the M&A took place (Kubo & Saito, 2012). The data were collected from the last annual reports of the acquirer and the target before the M&A took place.

(ii) Integration Stage. This stage refers to the year in which the M&A took place. The data of this stage are based on the performance of the acquirer, which already includes the performance of the target. The data were collected from the first annual report of the acquirer after the M&A took place. The annual reports (10-K) refer to 12 months, usually between January to December. Hence, the period of the integration stage could be between 12 months to 24 months, depending on the month that the M&A took place. This time lag is supposed to give a sufficient examination regarding the integration stage because this stage is expected to be shorter with the aim of consolidating operations to seize synergy potential as soon as possible. Therefore, if the integration stage extends beyond the period of 12-24 months as measured in this study, then it may signal that occur complications during the integration process, which hinder the ability to end successfully the integration stage at a reasonable time. Note, in some M&As, the integration stage begins at the due-diligence stage, such as the planning and even the restructuring of the organization before “day one” of the deal. Therefore, in some M&As of this study, the integration stage could be much longer than 12-24 months, if the integration process started in the pre-M&A stage. This study differs between integration success and integration failure, so the outcome of the integration stage, success or failure, should be affected by the planning, duration and effectiveness of the integration process.

(iii) Post-M&A Stage. This stage refers to the period after the M&A took place. The data of this stage are based on the performances of the acquirer, which already includes the performances of the target. The data were collected from the second annual report of the acquirer after the M&A took place. This time lag is supposed to give a satisfactory examination without the problems of a long-time lag after the M&A took place (Huber & Power, 1985). Adding additional years after the M&A took place, could violate the ‘clean data’ criterion (Ramaswamy, 1997) that may influence the assessment of M&A success, such as in cases where the acquirer buys additional targets during the long-term research period. In earlier studies, this criterion allowed a lag of more years after the M&A took place because fewer firms in the past bought more than one target shortly after the last deal. However, today, many firms buy more than one firm during a continuing year, and numerous firms buy several firms shortly after the last deal. This narrows the lag time of the years that should include in the M&A studies with the aim of fulfilling the ‘clean data’ criterion.

Measures

Mediator variable. The study included two variables as the mediator variables of the study, which refer to the outcomes of the integration process. These variables are based on the change in the revenue (in millions of US$) between the pre-M&A stage and the integration stage. The revenue represents the volume of activity and the value creation of the firms (Gates & Very, 2003). The nature of this change reflects the success or the failure of the integration stage and gives indications whether the volume of activity of the combined firm increased or decreased during the integration stage. The calculation of this measure is based on the last annual reports of the acquirer and the target before the M&A took place, as well as the first annual report of the acquirer after the M&A took place.

i. Integration Failure, Integration Stage. In this study, the integration process is considered a failure if the change in the revenue of the combined firm has a negative value. Therefore, this variable was defined as a dummy variable, where 1 represents integration failure in which the change in the revenue has a negative value, and 0 represents another.

ii. Integration Success, Integration Stage. In this study, the integration process is considered successful if the change in the revenue of the combined firm is above the average change of the revenue’s sample. This is based on the rationale that a positive minor change in the revenue can’t be considered as a success, unless it’s a significant positive change, at least above the average of the study. In this study, the average change in the revenue is 1,147 (in millions of US$), while the minimum is -7,458 and the maximum is 18,117, so minor change below the average can’t be considered as a success. Therefore, this variable was defined as a dummy variable, where 1 represents integration success in which the change in the revenue had a positive value above the average change of the revenue’s sample, and 0 represents another.

Dependent variables. The study included labour productivity as the dependent variable in this study, as follows:

Labour Productivity Change. Labour productivity is defined as a total output divided by labour inputs (Samuelson & Nordhaus, 1989). Therefore, in this study, this variable is based on the index ‘revenue per employees’ that calculates the revenue of the firm in relation to the overall number of workers (Datta et al., 2005; Huselid, 1995; Guthrie, 2001; Koch & McGrath, 1996), which examines the relative contribution of every worker in the achievement of the company’s overall income. The advantage of this measure is that it provides a single index that can be used to compare firms' productivity (Huselid, 1995). This current study examines the change in labour productivity between the pre-M&A stage and the post-M&A stage. Thus, the calculation of the change in labour productivity is based on the last annual reports of the acquirer and the target in the pre-M&A stage along with the second annual report of the acquirer after the M&A took place. Improvement in the labour productivity accrues, if the value of the revenue per employee of the combined firm after the M&A is greater than the sum of the values of the individual firms before the M&A took place.

Independent variables. The study included two independent variables that reflect the output and the input of the M&A, as follows:

i. Output - Synergy Success. The synergy success reflects the output of the M&A. In this study, the synergy success was examined using the change in the revenue (in millions of US$) between the pre-M&A stage and the post-M&A stage. The revenue represents the volume of activity and the value creation of the firms (Gates & Very, 2003). The calculation of the change in the revenue is based on the last annual reports of the acquirer and the target in the pre-M&A stage, as well as the second annual report of the acquirer after the M&A took place. Synergy is considered successful if the revenue of the combined firm in the post-M&A stage is greater than the sum of the revenue of the acquirer and the target before the M&A took place (Seth et al., 2002).

ii. Input - Workforce Change. The workforce change during the integration process reflects the input of the M&A. This variable was examined using the change in the number of employees between the pre-M&A stage and the integration stage. The calculation of the change in the workforce size is based on the last annual reports of the acquirer and the target in the pre-M&A stage, as well as the first annual report of the acquirer after the M&A took place.

Control variables. The study included four control variables that refer to the pre-M&A stage. These variables are based on the last annual reports of the acquirer and the target before the M&A took place, as follows:

i. Volume of Activity Ratio. The ratio is considered a useful indicator for assessing M&A strategy, particularly in relation to M&A performance (Kemal, 2011). This variable was examined using the revenue (in millions of US$) of the acquirer and the target in the pre-M&A stage. The revenue ratio is calculated by dividing the revenue value of the acquirer by the revenue value of the target (Hagedoorn & Duysters, 2002). Thus, a higher ratio implies a greater difference between the firms involved in the M&A. The existing literature confirms the argument that buying targets that are either very small or very large in relation to the acquirer can result in lower performances (Kitching, 1967; Moeller et al., 2004). Target that is too small in relation to the acquirer may not receive satisfactory attention from the management to realize the synergy potential (Kitching, 1967). However, when the target is very large in relation to the acquirer, then it’s more likely that this will lead to a political in-fighting because both the acquirer and the target struggle for dominance (Stahl et al., 2013). In addition, the integration process tends to be more complicated in cases of a larger target (Homberg et al., 2009), while similar size leads to the most efficient integration process (Ahuja & Katila, 2001) because it is less complicated to identify redundancies when both firms are of equal size (Krishnan et al., 2007). Therefore, a balance of size between the acquirer and the target is encouraging (Ahuja & Katila, 2001; Chung et al., 2000; Hagedoorn & Duysters, 2002)

ii. Labour Productivity Ratio. This variable is aimed to explore if the labour productivity ratio between the acquirer and the target in the pre-M&A stage influence the labour productivity in the post-M&A stage. This variable was examined using the ratio of the revenue per employee (in millions of US$) of the acquirer and the target in the pre-M&A stage. The measure of the revenue per employee is calculated by the value of the revenue divided by the number of employees (Piske, 2002) for each firm.

iii. Cross-border M&A. Cross-border M&A is defined as an M&A that the acquirer and the target originate from different countries. This variable is based on the status of the acquirer and the target before the M&A took place. This variable was defined as a dummy variable, where 1 represents cross-border M&A and 0 represents domestic M&A (O'Shaughnessy & Flanagan, 1998). Cross-border M&As have a high synergy potential (Seth et al., 2002) due to the differences between the geographic markets of the acquirer and the target, but the ability to seize synergies depends on the success of the integration process (Graebner, 2004; Weber et al., 2011). Thus, this study includes this variable with the aim of understanding if there is a difference between cross-border M&As and domestic M&As in relation to labour productivity.

iv. Labour Unions. This variable was defined as a dummy variable, where 1 represents an M&A with labour unions of the acquirer or the target or both, and 0 represents an M&A with no labour unions. This variable is based on the status of the acquirer and the target before the M&A took place. This variable is aimed to explore if an M&A with labour unions influence labour productivity in the post-M&A stage. On the one hand, the existing literature suggests that labour unions may contribute to productivity because unionized workers are more committed to the firm, as well as the labour unions may help to improve the communication between the workers and the management (Doucouliagos & Laroche, 2009; Laroche & Wechtler, 2011). On the other hand, inflexible working arrangements and industrial disputes may reduce the productivity in unionized firms (Hirsch, 1991). Besides, the main objective of the labour unions is to protect the workers against losing their jobs (Davidsson & Emmenegger, 2013), which may lead to political infighting between the labour unions and the management during the integration process. Given this consideration, the present study includes this variable as a control variable with the aim of shedding light on the influence of the labour unions on labour productivity in M&A activity.

Test Analysis

i. Hierarchical multiple regression. The study examined the hypotheses of the study, based on tests of a mediation model. There are several options to test a mediation model (Frazier et al., 2004; Wood et al., 2008). However, most of the existing studies in the literature were tested the mediation model based on the study of James and Brett (1984) (Frazier et al., 2004), despite the criticism in the literature regarding this testing (Frazier et al., 2004; Wood et al., 2008). As shown in Figure 3, a complete mediation model, X should affect Y indirectly through mediator M when the form of the model is X → M → Y (James & Brett 1984). In a mediation model, X represents the independent variables (here, the output and the input variables), M represents the mediating variables (here, the integration process variables) and Y represents the dependent variables (here, the labour productivity variable). According to James & Brett (1984), a mediation model should meet four conditions (Wood et al., 2008). Firstly, the independent variables should significantly account for the mediating variables (Path a) (Baron & Kenny, 1986). Secondly, the mediating variables should significantly account for the dependent variables (Path b) (Baron & Kenny, 1986). Thirdly, the independent variables should significantly account for the dependent variables (Path c) (Wood et al., 2008). Fourthly, when paths a and b are controlled, a previously significant relation between the independent and the dependent variables is no longer significant (Path c is zero) and is consistent with complete mediation, while a reduction in Path c is consistent with partial mediation (Baron & Kenny, 1986; Wood et al., 2008). In a complete mediation, the function has the form M = ƒ (X), Y = ƒ (M), while in a partial mediation, the function has the form M = ƒ (X), Y = ƒ (X, M) (James & Brett, 1984). The assumptions are confirmed when there is a significant R² increment because of the addition of the mediating variables (James & Brett, 1984). Hierarchical multiple regression as a structural equation is considered the preferred method for testing mediation models (Frazier et al., 2004; James & Brett, 1984), especially complex mediation models (Wood et al., 2008) that include a set of independent and mediating variables (Cohen et al., 2013; Frazier et al., 2004).

ii. VIF Test to Identify Multicollinearity Problem. The study included variance inflation factor (VIF) tests to identify multicollinearity problems (Mansfield & Helms, 1982). The multicollinearity is considered high if it is higher than 10, which reflects a multicollinearity problem (Chatterjee & Price, 1991; Hopkins & Ferguson, 2014). Therefore, the VIF index should be less than 10 (Chatterjee & Price, 1991; Hopkins & Ferguson, 2014). However, if the VIF values are over 5, then it can lead to problems regarding the interpreting of the regression results (Hair et al., 2011). Thus, VIF values between 5 and 10 are acceptable for screening of multicollinearity, but it should alert that interpretation of beta weights should be carefully assessed (Hopkins & Ferguson, 2014).

Results

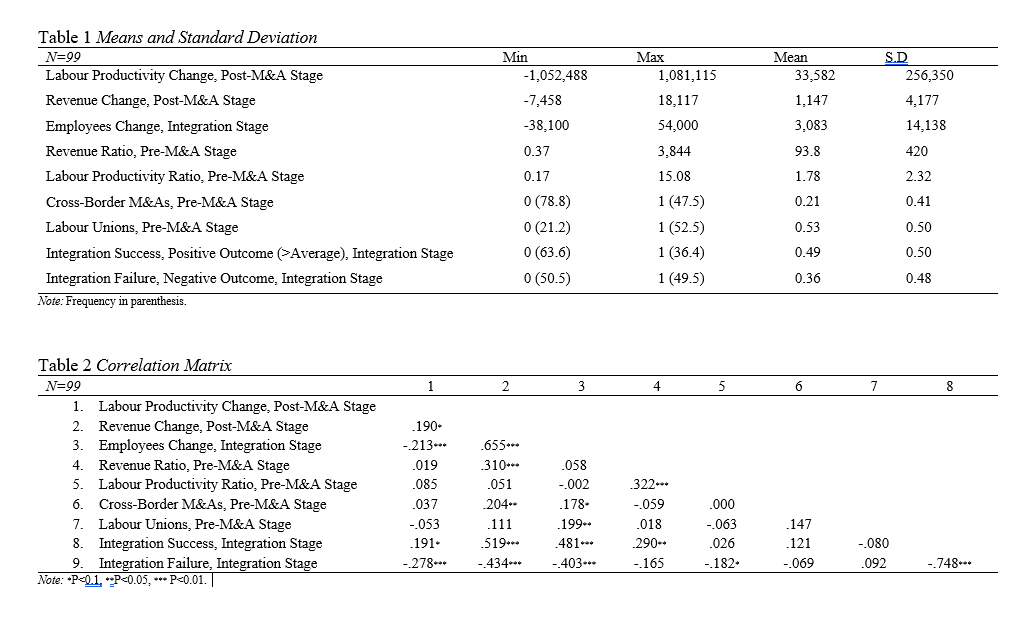

Table 1 shows the mean and descriptive statistics of the research variables. Table 2 shows the correlation matrix between the research variables. Table 3 shows the results of the hierarchical multiple regression. First, the results of the correlation matrix and the VIF test show that there is no multicollinearity problem between the research variables. There is a high correlation between the integration success and the integration failure variables, but these variables were tested separately. Second, the correlation matrix shows the results of path a and path b of the mediation model. These results confirm that there is a significant relationship between the mediator variable and the independent variables, as well as between the mediator variable and the dependent variable.

Step 1 in Table 3 shows the results of path c of the mediation model, which support hypotheses H1 and H2. The results show as expectedly that the synergy success as an output of the M&A is significantly and positively associated with labour productivity, while the workforce change as an input of the M&A is significantly and negatively associated with labour productivity.

Step 2 in Table 3 shows the results of path a+b of the mediation model, which support hypotheses H3-H6. As expectedly, the results show, that both integration success and integration failure mediate the relationship between the output and the input of the M&A and labour productivity. The results also show as expectedly that integration success is significantly and positively associated with labour productivity, while integration failure is significantly and negatively associated with labour productivity. Moreover, the results regarding the control variables show that only the volume of activity ratio is significantly and negatively associated with labour productivity, while the other control variable shows no significant results.

Discussion

The analysis of the study emphasizes the importance of this study. The study indicates that the nature of the M&A strategy is supposed to lead to a positive effect on labour productivity. The combination of synergy success and workforce reduction during the integration process is supposed to lead to an improvement in labour productivity. Realizing synergy potential leads to an increase in the output of the M&A, while the reduction of workforce size leads to a decrease in the input of the M&A, and as a result, it leads to an increase in labour productivity. This suggests that theoretically, an M&A strategy is supposed to lead to an improvement in labour productivity. However, the study highlights the differences between integration success and integration failure in relation to labour productivity. The study reveals that integration failure leads to a decline in labour productivity, while integration success leads to an improvement in labour productivity. These results confirm the argument in the existing literature that if the integration process was ended in a failure, it may negatively influence the performances of the M&A (Baunsgaard & Clegg, 2013; Chen & Wang, 2014; Mtar, 2010; Shimizu et al., 2004; Very et al., 1996; Yu et al., 2005).

Nevertheless, and even more importantly, the study reveals a mixed effect in relation to the integration success, which may explain the high failure rate of the M&A strategy. On the one hand, integration success positively influences the workforce size, but at the same time, it positively influences labour productivity. In other words, an increase in the workforce size helps to end successfully the integration process because there is no shortage in human resources to realize synergy potential, but at the same time, it hinders the ability to improve labour productivity. On the contrary, a decrease in the workforce size help to improve labour productivity, but it hinders the ability to end successfully the integration process. This confirms the argument of this study that the implementation of M&A strategy can create special conditions in relation to labour productivity due to the nature of the integration stage that leads to a problematic process in many M&As (Ahammad et al., 2012; Baunsgaard & Clegg, 2013; Calandro, 2008; Chen & Wang, 2014; Jemison & Sitkin, 1986; Krishnan et al., 2007; Krishnan & Park, 2002; Kroon et al., 2015; Krug & Nigh, 2001; Lehto & Böckerman, 2008; Lubatkin et al., 1999; Mtar, 2010; Piske, 2002; Schweizer, 2005; Shaver, 2006; Shimizu et al., 2004; Very et al., 1996; Weber et al., 2011, 2012; Yu et al., 2005). This may explain the high failure rate of M&A strategy because of the challenges to achieve both synergy success and an improvement in labour productivity. This phenomenon needs to be addressed in additional studies in the future.

Conclusions

Due to the high failure rate of the M&A strategy (Alkaraan, 2019; Jap et al., 2017; Kumar & Sharma, 2019; Renneboog & Vansteenkiste, 2019; Rozen-Bakher, 2018c, 2018d; Thelisson, 2020; Venema, 2015; Wangerin, 2019; Weber et al., 2012), this study raises the question if the M&A strategy can lead to a creation of special conditions in relation to labour productivity due to the integration process. Labour productivity is considered a crucial organizational outcome (Datta et al., 2005) and it has defined as the total output divided by labour inputs (Samuelson & Nordhaus, 1989), which indicates the efficiency of the labour force in creating the output of the firm (Datta et al., 2005). However, when a firm implements an M&A strategy, it could lead to special conditions in relation to labour productivity due to the nature of the integration process. Under conditions of M&A strategy, if a firm reduces its number of workers during the integration process with the aim of eliminating duplicate jobs, overlapping activities (Lehto & Böckerman, 2008) and consolidation of functions to remove redundancies (Krishnan & Park, 2002), then it may hinder the ability to seize synergies due to the shortage in employees, and consequently, it may negatively influence the labour productivity. However, despite the importance of labour productivity (Datta et al., 2005), the M&A literature lacks both theoretical and empirical studies regarding labour productivity. More specifically, the M&A literature doesn’t provide theoretical background if there is a difference between labour productivity under conditions of M&A strategy and under normal conditions when the firm doesn’t involve in M&As.

In the light of the above, this study presents a mediation model with the aim of exploring if the integration process mediates the relationship between the output (synergy success) and the input (workforce change during the integration process) of the M&A and labour productivity in the post-M&A period. The sample of the study included 198 public firms from 10 countries that were involved in M&A activity in the industry sector. The study is based on the accounting research method. This method is considered the preferred method for comparing the changes in performances during the M&A process because it focuses on the past performances (Seth, 1990), which allow exploring the real outcomes of the M&A in the post-M&A period. Therefore, the study database was based on 396 annual reports (10-K) of the public firms included in the sample. These reports are considered a reliable source for the performances of the firms.

The results of the study show that the combination of synergy success along with the reduction of workforce size during the integration stage leads to an improvement in labour productivity in the post-M&A period. This suggests that seizing synergy leads to an increase in the output of the M&A, while the reduction of workforce size leads to a decrease in the input of the M&A, and as a result, it leads to an increase in labour productivity. The results also show that both integration success and integration failure mediate the relationship between the output and the input of the M&A and labour productivity in the post-M&A period. However, the results show differences between the two mediator variables in relation to labour productivity. Integration success leads to an improvement in labour productivity, while integration failure leads to a decline in labour productivity. These results highlight the novelty of this research because it confirms the assumption of this study that M&A strategy can lead to the creation of special conditions in relation to labour productivity due to the integration process. On the one hand, the nature of the M&A strategy is supposed to lead to a positive effect on labour productivity if the integration process ended in success. On the other hand, if the integration process ended in failure, then it harms labour productivity. Nevertheless, and even more importantly, the study reveals a mixed effect in relation to integration success. The results show that integration success positively influences the workforce size, but at the same time, it positively influences labour productivity. This suggests that an increase in the workforce size help to end successfully the integration process because there is no a shortage in the human resource to realize synergy potential, but at the same time, it hinders the ability to improve the labour productivity. On the contrary, a decrease in the workforce size help to improve labour productivity, but it hinders the ability to successfully end the integration process. This mixed effect may explain the high failure rate of M&A strategy because it shows the challenges in achieving both synergy success and an improvement in labour productivity in M&As. This highlights the trade-off that may exist between synergy and efficiency in M&A strategy.

Limitations of the Study and Future Research

The main limitation of this study stems from the lack of previous studies that explore the relationship between labour productivity and M&A activity. Therefore, this study emphasises the need for future research with the aim of developing a well-grounded theoretical foundation regarding the influence of M&A strategy on labour productivity. Emphasis should be given to the question of whether the M&A strategy creates special conditions in relation to labour productivity due to the nature of the integration process. Additionally, this study focuses on the industry sector because of the expectation of the decline in the ratio of employees engaged in production (Clark, 1940). Hence, this study emphasises the need for future research that examine the labour productivity in different sector like the services sector. Furthermore, at the methodology level, this study used the index of revenue per employee to examine labour productivity. Thus, future studies should be used additional measures, such as profits per employee (Bryan, 2007) or TEF (Ferrier & Valdmanis, 2004; Harris & Robinson, 2002; Karpaty, 2007) Moreover, this study emphasises the need for future research that examine the labour productivity in different types of M&A, such as conglomerate or horizontal M&As (Tremblay & Tremblay, 2012). Finally, the labour productivity could be affected by a variety of factors such as the scope of activity, technological advantages (Cobet & Wilson, 2002), skilled workers (Aggrey et al., 2010), management education and training (Aggrey et al., 2010), lack of workers (Aggrey et al., 2010), lack of labour experience (Enshassi et al., 2007), lack of labour surveillance (Enshassi et al., 2007), misunderstanding between labour and superintendents (Enshassi et al., 2007), labour disloyalty (Enshassi et al., 2007), work practices (Cappelli & Neumark, 2001; Huselid, 1995; Guthrie, 2001), etc. Hence, this study raises the need for future studies with the aim of examining which of these factors may influence labour productivity in M&As. These factors could be included in future studies as antecedent factors or as control variables.

References

Aggrey, N., Eliab, L., & Joseph, S. (2010). Human capital and labor productivity in East African manufacturing firms. Current Research Journal of Economic Theory, 2(2), 48-54.

Ahammad, M. F., Glaister, K. W., Weber, Y., & Tarba, S. Y. (2012). Top management retention in cross-border acquisitions: the roles of financial incentives, acquirer’s commitment and autonomy. European Journal of International Management, 6(4), 458-480.

Ahuja, G., & Katila, R. (2001). Technological acquisitions and the innovation performance of acquiring firms: A longitudinal study. Strategic management journal, 22(3), 197-220.

Alkaraan, F. (2019). Making M&A Less Risky: The Influence of Due Diligence Processes on Strategic Investment Decision Making'. Advances in Mergers and Acquisitions (Volume 18). Emerald Publishing Limited, 99-110.

Angwin, D., & Savill, B. (1997). Strategic perspectives on European cross-border acquisitions: A view from top European executives. European Management Journal, 15(4), 423-435.

Baron, R. M., & Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of personality and social psychology, 51(6), 1173.

Baunsgaard, V. V., & Clegg, S. (2013). ‘Walls or boxes’: The effects of professional identity, power and rationality on strategies for cross-functional integration. Organization Studies, 34(9), 1299-1325.

Bryan, L. L. (2007). The new metrics of corporate performance: Profit per employee. McKinsey Quarterly, 1, 56.

Caiazza, R., & Volpe, T. (2015). M&A process: A literature review and research agenda. Business Process Management Journal, 21(1), 205-220.

Calandro, J. J. (2008). Assessing the risk of M&A: Bruner's Disaster Framework applied to Berkshire Hathaway's Gen Re Acquisition. Strategy & Leadership, 36, 20-27.

Calipha, R., Tarba, S., & Brock, D. (2010). Mergers and acquisitions: a review of phases, motives, and success factors. Advances in mergers and acquisitions, 9(1), 1-24.

Cappelli P. 2000. Examining the incidence of downsizing and its effect on establishment performance. In D. Neumark (Ed), On the job: Is long-term employment a thing of the past: 463–516. New York: Russell Sage Foundation.

Cappelli, P., & Neumark, D. 2001. Do “high-performance” work practices improve establishment-level outcomes? Industrial and Labor Relations Review, 54, 737–775.

Carpenter, M.A., & Sanders, W.G. (2007). Strategic management: A dynamic perspective. Upper Saddle River, NJ: Pearson Prentice Hall.

Chakravarthy, B. S. (1986). Measuring strategic performance. Strategic management journal, 7(5), 437-458.

Changjun, Y., & Qiaoyue, L. (2014). The study of the performance of manufacturing enterprises cross-border M&A in China based on super-efficiency DEA. Journal of Chemical and Pharmaceutical Research, 6, 1942-1945.

Chatterjee, S., & Price, B. (1991). Regression diagnostics. New York.

Chen, F., & Wang, Y. (2014). Integration risk in cross-border M&A based on internal and external resource: empirical evidence from China. Quality & Quantity, 48(1), 281-295.

Chung, S. A., Singh, H., & Lee, K. (2000). Complementarity, status similarity and social capital as drivers of alliance formation. Strategic management journal, 21(1), 1-22.

Clark, C. 1940. The Conditions of Economic Progress. London: MacMillan and Co. Ltd.

Cobet,A,E & Wilson,G,A. 2002. Comparing 50 years of labor productivity in U.S and foreign manufacturing. Monthly Labor Review, June, 51-65.

Cohen, J., Cohen, P., West, S. G., & Aiken, L. S. (2013). Applied multiple regression/correlation analysis for the behavioral sciences. Routledge.

Conyon, M., Girma, S., Thompson, S., & Wright, P. (2002). The impact of foreign acquisition on wages and productivity in the UK. Journal of Industrial Economics, 50(1), 85-102.

Datta, D. K., Guthrie, J. P., & Wright, P. M. (2005). Human resource management and labor productivity: does industry matter?. Academy of management Journal, 48(1), 135-145.

Davidsson, J. B., & Emmenegger, P. (2013). Defending the organisation, not the members: Unions and the reform of job security legislation in Western Europe. European Journal of Political Research, 52(3), 339-363.

Deakin, S., & Slinger, G. (1997). Hostile takeovers, corporate law, and the theory of the firm. Journal of Law and Society, 24(1), 124-151.

Delery, J. E., & Shaw, J. D. 2001. The strategic management of people in work organizations: Review, synthesis and extension. In K. M. Rowland & G. R. Ferris (Eds). Research in personnel and human resource management, 165–197. Greenwich, CT: JAI Press.

Doucouliagos, H., & Laroche, P. (2009). Unions and Profits: A Meta‐Regression Analysis1. Industrial relations: a journal of economy and society, 48(1), 146-184.

Dyer, L., & Reeves, T. (1995). Human resource strategies and firm performance: what do we know and where do we need to go?. International Journal of human resource management, 6(3), 656-670.

Enshassi, A., Mohamed, S., Mustafa, Z. A., & Mayer, P. E. (2007). Factors affecting labour productivity in building projects in the Gaza Strip. Journal of Civil Engineering and Management, 13(4), 245-254.

Ferrier, G. D., & Valdmanis, V. G. (2004). Do mergers improve hospital productivity?. Journal of the Operational Research Society, 55(10), 1071-1080.

Frazier, P.A., Tix, A.P., Barron, K.E. (2004). Testing moderator and mediator effects in counseling psychology research. Journal of counseling psychology, 51, 115-134.

Freeman, S. J., & Cameron, K. S. (1993). Organizational downsizing: A convergence and reorientation framework. Organization Science, 4(1), 10-29.

Froud, J., Haslam, C., Johal, S., & Williams, K. (2000). Restructuring for shareholder value and its implications for labour. Cambridge Journal of Economics, 24(6): 771-797.

Gates, S., & Very, P. (2003). Measuring performance during M&A integration. Long Range Planning, 36(2), 167-185.

Gibbs, P. A. (1993). Determinants of corporate restructuring: the relative importance of corporate governance, takeover threat and free cash flow. Strategic Management Journal, 14, Special Issue, 51–68.

Gordon, R. J. (2016). The rise and fall of American growth: The US standard of living since the civil war. Princeton University Press.

Graebner, M. E. (2004). Momentum and serendipity: How acquired leaders create value in the integration of technology firms. Strategic Management Journal, 25(8‐9), 751-777.

Guthrie, J. P. (2001). High-involvement work practices, turnover, and productivity: Evidence from New Zealand. Academy of Management Journal, 44, 180 – 190

Hagedoorn, J., & Duysters, G. (2002). The effect of mergers and acquisitions on the technological performance of companies in a high-tech environment. Technology Analysis & Strategic Management, 14(1), 67-85.

Hair, J. F., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal of Marketing theory and Practice, 19(2), 139-152.

Hambrick, D. C., & Cannella, A. A. (1993). Relative standing: A framework for understanding departures of acquired executives. Academy of Management journal, 36(4), 733-762.

Harris, R., & Robinson, C. (2002). The effect of foreign acquisitions on total factor productivity: plant-level evidence from UK manufacturing, 1987–1992. Review of Economics and Statistics, 84(3), 562-568.

Haspeslagh, P. C., & Jemison, D. B. (1991). Managing acquisitions: Creating value through corporate renewal (Vol. 416). New York: Free Press.

Hirsch, B. T. (1991). Union coverage and profitability among US firms. The review of economics and statistics, 69-77.

Hitt, M. A., Bierman, L., Shimizu, K., & Kochhar, R. (2001). Direct and moderating effects of human capital on strategy and performance in professional service firms: a resource-based perspective. Academy of Management Journal, 44, 13–28.

Homberg, F., Rost, K., & Osterloh, M. (2009). Do synergies exist in related acquisitions? A meta-analysis of acquisition studies. Review of Managerial Science, 3(2), 75-116.

Hopkins, L., & Ferguson, K. E. (2014). Looking forward: The role of multiple regression in family business research. Journal of Family Business Strategy, 5(1), 52-62.

Huber, G. P., & Power, D. J. (1985). Retrospective reports of strategic‐level managers: Guidelines for increasing their accuracy. Strategic management journal, 6(2), 171-180.

Huselid, M. A. 1995. The impact of human resource management practices on turnover, productivity, and corporate financial performance. Academy of Management Journal, 38, 635– 672.

Iverson, R. D., & Zatzick, C. D. (2011). The effects of downsizing on labor productivity: The value of showing consideration for employees' morale and welfare in high‐performance work systems. Human Resource Management, 50(1), 29-44.

James, L. R., & Brett, J. M. (1984). Mediators, moderators, and tests for mediation. Journal of Applied Psychology, 69(2), 307-321.

Jap, S., Gould, A. N., & Liu, A. H. (2017). Managing mergers: Why people first can improve brand and IT consolidations. Business Horizons, 60(1), 123-134.

Jemison, D. B., & Sitkin, S. B. (1986). Corporate acquisitions: A process perspective. Academy of Management Review, 11, 145-163.

John, K., Knyazeva, A., & Knyazeva, D. (2015). Employee rights and acquisitions. Journal of Financial Economics, 118, 49-69.

Kane, T. 2010. The importance of startups in job creation and job destruction. Kauffman Foundation Research Series: Firm Formation and Economic Growth.

Karpaty, P. (2007). Productivity effects of foreign acquisitions in Swedish manufacturing: The FDI productivity issue revisited. International Journal of the Economics of Business, 14(2), 241-260.

Kemal, M. U. (2011). Post-merger profitability: A case of Royal Bank of Scotland (RBS). International Journal of Business and Social Science, 2(5), 157-162.

King, D. R., Dalton, D. R., Daily, C. M., & Covin, J. G. (2004). Meta‐analyses of post‐acquisition performance: Indications of unidentified moderators. Strategic management journal, 25(2), 187-200.

Kitching, J. (1967). Why do mergers miscarry. Harvard Business Review,45(6), 84-101.

Koch, M. J., & McGrath, R. G. (1996). Improving labor productivity: Human resource management policies do matter. Strategic Management Journal, 17, 335– 354.

Krishnan, H. A., & Park, D. (2002). The impact of work force reduction on subsequent performance in major mergers and acquisitions: an exploratory study. Journal of Business Research, 55(4), 285-292.

Krishnan, H. A., Hitt, M. A., & Park, D. (2007). Acquisition premiums, subsequent workforce reductions and post‐acquisition performance. Journal of Management Studies, 44(5), 709-732.

Kroon, D. P., Cornelissen, J. P., & Vaara, E. (2015). Explaining employees’ reactions towards a cross-border merger: the role of English language fluency. Management International Review, 55(6), 775-800.

Krug, J. A., & Nigh, D. (2001). Executive perceptions in foreign and domestic acquisitions: An analysis of foreign ownership and its effect on executive fate. Journal of World Business, 36(1), 85-105.

Kubo, K., & Saito, T. (2012). The effect of mergers on employment and wages: Evidence from Japan. Journal of The Japanese and International Economies, 26, 263-284.

Kumar, V., & Sharma, P. (2019). Why Mergers and Acquisitions Fail?. In An Insight into Mergers and Acquisitions (pp. 183-195). Palgrave Macmillan, Singapore.

Laroche, P., & Wechtler, H. (2011). The effects of labor unions on workplace performance: New evidence from France. Journal of labor research, 32(2), 157-180.

Larsson, R., & Finkelstein, S. (1999). Integrating strategic, organizational, and human resource perspectives on mergers and acquisitions: A case survey of synergy realization. Organization Science, 10, 1–26.

Lehto, E., & Böckerman, P. (2008). Analysing the employment effects of mergers and acquisitions. Journal of Economic Behavior & Organization, 68(1), 112-124.

Lichtenberg, F. R., Siegel, D., Jorgenson, D., & Mansfield, E. (1987). Productivity and changes in ownership of manufacturing plants. Brookings Papers on Economic Activity, 1987(3), 643-683.

Liu, X., Parker, D., Vaidya, K. & Wei, Y. (2001). The impact of foreign direct investment on labour productivity in the Chinese electronics Industry. International Business Review, 10, 421–439.

Lubatkin, M. (1983). Mergers and the Performance of the Acquiring Firm. Academy of Management review, 8(2), 218-225.

Lubatkin, M. (1987). Merger strategies and stockholder value. Strategic management journal, 8(1), 39-53.

Lubatkin, M., Schweiger, D., & Weber, Y. (1999). Top Management Turnover M Related M&A’s: An Additional Test of the Theory of Relative Standing. Journal of Management, 25(1), 55-73.

Mahmood, M. (2008). Labour productivity and employment in Australian manufacturing SMEs. International Entrepreneurship and Management Journal, 4(1), 51-62.

Mansfield, E. R., & Helms, B. P. (1982). Detecting multicollinearity. The American Statistician, 36(3a), 158-160.

McGuckin, R. H., & Nguyen, S. V. (2001). The impact of ownership changes: A view from labor markets. International Journal of Industrial Organization, 19(5), 739-762.

Mitchell, W., & Shaver, J. M. (2003). Who buys what? How integration capability affects acquisition incidence and target choice. Strategic Organization, 1(2), 171-201.

Moeller, S. B., Schlingemann, F. P., & Stulz, R. M. (2004). Firm size and the gains from acquisitions. Journal of Financial Economics, 73(2), 201-228.

Mtar, M. (2010). Institutional, industry and power effects on integration in cross-border acquisitions. Organization Studies, 31(8), 1099-1127.

NASDAQ, Nasdaq Stock Market. (2021). Nasdaq Stock Market. https://business.nasdaq.com/

NYSE, New York Stock Exchange. (2021). New York Stock Exchange https://www.nyse.com/index

Oler, D. K., Harrison, J. S., & Allen, M. R. (2008). The danger of misinterpreting short-window event study findings in strategic management research: an empirical illustration using horizontal acquisitions. Strategic Organization, 6(2), 151-184.

Oler, D. K., Harrison, J. S., & Allen, M. R. (2008). The danger of misinterpreting short-window event study findings in strategic management research: an empirical illustration using horizontal acquisitions. Strategic Organization, 6(2), 151-184.

O'Shaughnessy, K. C., & Flanagan, D.J. (1998). Determinants of layoff announcements following M&As: An empirical investigation. Strategic management journal, 19(10), 989-999.

Pablo, A. L. (1994). Determinants of acquisition integration level: A decision-making perspective. Academy of management Journal, 37(4), 803-836.

Piske, R. (2002). German acquisitions in Poland: an empirical study on integration management and integration success. Human Resource Development International, 5, 295-312.

Porter, M. E. (1985). Competitive advantage. New York: Free Press.

Puranam, P., Powell, B. C., & Singh, H. (2006). Due diligence failure as a signal detection problem. Strategic Organization, 4(4), 319-348.

Ramaswamy, K. (1997). The performance impact of strategic similarity in horizontal mergers: Evidence from the US banking industry. Academy of Management Journal, 40(3), 697-715.

Renneboog, L., & Vansteenkiste, C. (2019). Failure and success in mergers and acquisitions. Journal of Corporate Finance, 58, 650-699.

Rhoades, S. A. (1998). The efficiency effects of bank mergers: An overview of case studies of nine mergers. Journal of Banking & Finance, 22, 273-291.

Rozen-Bakher Z. (2018a). Comparison of Merger and Acquisition (M&A) Success in Horizontal, Vertical and Conglomerate M&As: Industry Sector vs. Services Sector’. The Service Industries Journal 38(7-8), 492-518. DOI: 10.1080/02642069.2017.1405938.

Rozen-Bakher, Z. (2017). Impact of Inward and Outward FDI on Employment: The Role of Strategic Asset-Seeking FDI. Transnational Corporations Review, 9(1), 16-30.

Rozen-Bakher, Z. (2018b). How does the dimensions of Hofstede’s national cultural influence cross-border M&As success?. Transnational Corporations Review, 1-16. Published online on 24 May 2018. DOI:10.1080/19186444.2018.1475089

Rozen-Bakher, Z. (2018c). The Trade-off Between Synergy Success and Efficiency Gains in M&A Strategy. EuroMed Journal of Business, 13(2), 163-184.

Rozen-Bakher, Z. (2018d). Could the pre-M&A performances Predict Integration Risk in Cross-Border M&As? International Journal of Organizational Analysis. DOI: 10.1108/IJOA-07-2017-1199.

Samuelson, P. A., & Nordhaus, W. D. (1989). Economics (13th ed.). New York: McGraw-Hill.

Sarala, R. M. (2010). The impact of cultural differences and acculturation factors on post-acquisition conflict. Scandinavian Journal of Management, 26(1), 38-56.

Schettkat, R., & Yocarini, L. (2006). The shift to services employment: A review of the literature. Structural change and economic dynamics, 17(2), 127-147.

Schweizer, L. (2005). Organizational integration of acquired biotechnology companies into pharmaceutical companies: The need for a hybrid approach. Academy of Management Journal, 48(6), 1051-1074.

SEC, U.S. Securities and Exchange Commission. 2021. https://www.sec.gov/fast-answers/answers-form10khtm.html

Seth, A. (1990). Value creation in acquisitions: A re‐examination of performance issues. Strategic Management Journal, 11(2), 99-115.

Seth, A., Song, K. P., & Pettit, R. R. (2002). Value creation and destruction in cross‐border acquisitions: an empirical analysis of foreign acquisitions of US firms. Strategic management journal, 23(10), 921-940.

Shaver, J. M. (2006). A paradox of synergy: Contagion and capacity effects in mergers and acquisitions. Academy of Management Review, 31(4), 962-976.

Shimizu, K., Hitt, M. A., Vaidyanath, D., & Pisano, V. (2004). Theoretical foundations of cross-border mergers and acquisitions: A review of current research and recommendations for the future. Journal of International Management, 10(3), 307-353.

Stahl, G. K., & Voigt, A. (2008). Do cultural differences matter in mergers and acquisitions? A tentative model and examination. Organization Science, 19(1), 160-176.

Stahl, G. K., Angwin, D. N., Very, P., Gomes, E., Weber, Y., Tarba, S. Y., ... and Durand, M. (2013). Sociocultural integration in mergers and acquisitions: Unresolved paradoxes and directions for future research. Thunderbird International Business Review, 55(4), 333-356.

Steger, U., & Kummer, C. (2007). Why merger and acquisition (M&A) waves reoccur: the vicious circle from pressure to failure. IMD.

Thelisson, A. S. (2020). Managing failure in the merger process: evidence from a case study. Journal of Business Strategy.

Tichy, G. (2001). What do we know about success and failure of mergers?. Journal of Industry, Competition and Trade, 1(4), 347-394.

Tremblay, V. J., & Tremblay, C. H. (2012). Horizontal, Vertical, and Conglomerate Mergers. In New Perspectives on Industrial Organization (pp. 521-566). Springer New York.

Venema, W. H. (2015). Integration: The Critical M&A Success Factor. Journal of Corporate Accounting & Finance, 26(4), 23-27.

Vennet, R. V. (1996). The effect of mergers and acquisitions on the efficiency and profitability of EC credit institutions. Journal of Banking & Finance, 20, 1531-1558.

Very, P., Lubatkin, M., & Calori, R. (1996). A cross-national assessment of acculturative stress in recent European mergers. International Studies of Management & Organization, 26(1), 59-86.

Wangerin, D. (2019). M&A due diligence, post‐acquisition performance, and financial reporting for business combinations. Contemporary Accounting Research, 36(4), 2344-2378.

Weber, Y., Shenkar, O., & Raveh, A. (1996). National and corporate cultural fit in mergers/acquisitions: An exploratory study. Management science,42(8), 1215-1227.

Weber, Y., Tarba, S.Y., Rozen-Bachar, Z. (2011). Mergers and acquisitions performance paradox: The mediating role of integration approach. European Journal of International Management, 5, 373-393.

Weber, Y., Tarba, S.Y., Rozen-Bachar, Z. (2012). The effects of culture clash on international mergers in the high tech industry. World Review of Entrepreneurship, Management and Sustainable Development, 8: 103-118.

Wood, R. E., Goodman, J. S., Beckmann, N., & Cook, A. (2008). Mediation testing in management research a review and proposals. Organizational research methods, 11(2), 270-295.

Yanadori, Y., & Kato, T. (2007). Average employee tenure, voluntary turnover ratio, and labour productivity: Evidence from Japanese firms. The International Journal of Human Resource Management, 18(10), 1841-1857.

Yu, J., Engleman, R. M., & Van de Ven, A. H. (2005). The integration journey: An attention-based view of the merger and acquisition integration process. Organization studies, 26(10), 1501-1528.

Zollo, M., & Meier, D. (2008). What is M&A performance?. The Academy of Management Perspectives, 22(3), 55-77.