PS3 - Research Paper. Rozen-Bakher, Z. Do Labour Unions Lead to a Failure of Mergers and Acquisitions?: Game Theory Analysis

Rozen-Bakher, Z. Do Labour Unions Lead to a Failure of Mergers and Acquisitions?: Game Theory Analysis Research Paper, PS3. https://www.rozen-bakher.com/research-papers/ps3

COPYRIGHT ©2019-2024 ZIVA ROZEN-BAKHER ALL RIGHTS RESERVED

Rozen-Bakher, Z.

Do Labour Unions Lead to a Failure of Mergers & Acquisitions (M&As)?: Game Theory Analysis

Abstract

This study raises the question of whether labour unions lead to a failure of Mergers & Acquisitions (M&As) due to the political infighting during the integration stage between the players, namely: management, buyer’s union and seller’s union. The study used the Game Theory to explain the non-cooperative games that arise between the players during the integration stage. The study presents a novel set of labour unions variables: the buyer’s union, the seller’s union, M&As with one union (buyer or seller), M&As with two unions (buyer and seller) and M&As without labour unions. The results show that an M&A with two labour unions leads to a ‘lose-lose scenario’ that indicates a negative influence on both the revenue and profitability. The study suggests that an M&A with two labour union leads to conflicts during the integration stage due to the ability to form a coalition between two players against a third player, which negatively influence the M&A performance. Nevertheless, the study reveals that an M&A with one labour union, especially the seller’s union leads to a ‘win-win scenario’ that reflect a positive influence on both the revenue and profitability. The study concludes that an M&A with two labour unions (buyer and seller) has a high risk for failure, while an M&A with one labour union (buyer or seller) creates opportunities for success. The study highlights the importance of using Game theory to explain the political infighting between the labour unions.

Keywords: Firm Performance; Game Theory; Labour Unions; Mergers and Acquisitions (M&As); Risk Management

Introduction

The M&A literature strives to explain the high failure rate of Merger and Acquisition (M&A) strategy (King et al., 2004; Kumar & Sharma, 2019; Matsumoto, 2019; Renneboog & Vansteenkiste, 2019; Rozen-Bakher, 2018c; Sarala, 2010; Steger & Kummer, 2007; Tichy, 2001; Venema, 2015; Thelisson, 2020; Weber et al., 2012), particularly in relation to the invisible factors in the financial statements of the firms (e.g. invisible factors like labour unions vs. visible factors like net profit). Hence, this study raises the question if the labour unions lead to a failure of M&As due to the political infighting during the integration stage between the players, namely: management, buyer’s union and seller’s union.

The integration stage serves as a ‘bridge’ between the pre-M&A period and the post-M&A period (Rozen-Bakher, 2018d). The integration process aims at creating a consolidation of the combined firms in relation to the functional activities, organizational structure and culture of the firms (Pablo, 1994; Rozen-Bakher, 2018a; Stahl & Voigt, 2008). However, the integration stage is considered as the ‘weakest link’ of the M&A strategy (Rozen-Bakher, 2018d), and many previous studies highlight its negative implications on the organizations (e.g. Baunsgaard & Clegg, 2013; Chen & Wang, 2014; Mtar, 2010; Shimizu et al., 2004; Rozen-Bakher, 2018c; Very et al., 1996; Yu et al., 2005). More importantly, the dramatic implication of the integration is related to the workforce reduction (Deakin & Slinger, 1997; Gibbs, 1993; Haspeslagh & Jemison, 1991; Lehto & Böckerman, 2008; O’Shaughnessy & Flanagan, 1998; Rozen-Bakher, 2018d), particularly when involving a labour union in the deal. The labour unions aspire to secure the jobs of the workers, which leads to a conflict with the management who tries to maximize the efficiency (Becker & Olson, 1989; Palokangas, 1996). This conflict escalates in M&As, particularly if a labour union actively resists the reduction of jobs through slowdowns and strikes, which deters the management to cut jobs (Adams & Neely, 2000), and as a result, it may negatively influence the M&A success (Hirsch, 1991). Hence, the main concern of the managers who engage in the M&A activity if M&As with labour unions may lead to a ‘lose-lose trade-off scenario’ of the M&A strategy (Rozen-Bakher, 2018d), and as a result to a failure of M&A.

Despite the importance of this concern, the M&A literature lacks studies that examine the influence of labour unions on M&A performance, particularly during integration success, especially by new studies. There are previous studies that examined the influence of the labour unions on M&A activity (e.g. Armah & Peoples, 1997; Becker & Olson, 1989; Chen et al., 2011, 2012; Doucouliagos & Laroche, 2009; Fallick & Hassett, 1996; Heywood & Peoples, 1994; John et al., 2015; Lee & Mas, 2012; Lommerud et al., 2006; Lommerud et al., 2011; Rosett, 1990; Zeller, 2000). However, these studies mainly investigated the power of the labour unions (e.g. Fallick & Hassett, 1996; John et al., 2015) and the financial costs of the labour unions in relation to M&A activity (e.g. Chen et al., 2011, 2012; Lee & Mas, 2012), rather than to investigate the influence of the labour unions on M&A performance. Furthermore, the existing literature lacks studies that compare the buyer’s union and the seller’s union in relation to M&A performance during the integration stage. Comparing the buyer’s union and the seller’s union can help to explain which union, buyer or seller, has a greater impact on M&A performance during the integration stage. Even comparing between M&As with one union (buyer or seller) and M&As with two unions (buyer and seller), lack examination in previous studies. This comparison is particularly important, because it may help to determine whether M&As with two labour unions lead to more conflicts during the integration process compare to M&As with one labour union, and as a result, hinder the M&A performance at the integration stage. Moreover, the M&A literature lacks studies that examine the labour union as a mediator variable between the types of M&A and M&A performances. Each type of M&A (e.g. vertical M&A or horizontal M&A) has a unique challenge (Rozen-Bakher, 2018a; Tremblay & Tremblay, 2012), particularly if a labour union is involved in the integration process. Therefore, needed two layers of understanding in relation to the role of labour unions in M&As. The first layer should focus on the investigation if the labour unions influence M&A performance. The second layer should deal with the differences between the types of M&As when a labour union is involved in the deal. The second layer may help to reveal the invisible factors that cannot be seen in the financial statements of the seller, nor the ‘financial matching’ between the buyer and the seller. This may help to identify which type of M&A has a high vulnerability for failure when a labour union is involved in the integration process.

Considering the outline above, this study strives to fill these research gaps. Therefore, this study developed a mediating research model to explore how the labour unions mediate the relationship between the type of M&A and M&A performance during the integration stage. Based on the M&A literature, hypotheses are developed and tested using a sample of 197 public buyers and 197 public sellers from 13 countries that have traded on NASDAQ and NYSE.

In light of the introduction above, the study includes an additional seven sections, as follows: The first section outlines the theoretical background and hypotheses. The second section deals with the methodology of the study. The third and fourth sections present and discuss the results. The fifth section presents the conclusions and discusses the implications for decision-makers. The final section discusses the limitations of the study and gives recommendations for future studies.

Theoretical Background and Hypotheses

This study presents a mediating research model to explain how the labour unions mediate the relationship between the type of M&A and the M&A performance during the integration stage, as shown in Figure 1. The research model comprises five mediator variables ─ M&As without unions, buyer’s union, seller’s union, M&As with one union (buyer or seller) and M&As with two unions (buyer and seller) ─ to examine how each of them separately influences M&A performance. The research model also includes three types of M&As − cross-border, horizontal and vertical M&As. These types reflect the differences between the types of M&A regarding the complexity of the integration process when a labour union is involved in the deal. The theoretical background and the development of the hypotheses are presented and discussed in this section below.

The Role of the Labour Unions in M&As: The Game Theory Analysis

An M&A with Labour union versus an M&A without Labour Union. Based on a synthesis of two bodies of literature, the M&A literature and the labour union literature, it can be argued that labour unions may hinder M&A performance, particularly during the integration stage. The management and the labour unions have in general conflicts (John et al., 2015), especially when the firm involves in M&A (Lommerud et al., 2006), because of the need to cut jobs during the integration, as part of the implementation of M&A strategy. In other words, the objective of the management is to reduce jobs during the integration stage (Deakin & Slinger, 1997; Gibbs, 1993; Haspeslagh & Jemison, 1991; Lehto & Böckerman, 2008; O’Shaughnessy & Flanagan, 1998; Rozen-Bakher, 2018c), while the objective of the labour unions is to protect the workers from losing their jobs (Davidsson & Emmenegger, 2013). This conflict of objectives can lead to industrial relations disputes between the management and the labour unions, particularly if needed a massive reduction of jobs during the integration stage. Golden (1997) argues that the labour unions resist cutting jobs, particularly if exist a threat to the power and survival of the labour union due to the reduction of the workforce.

In light of that, the elimination of jobs during the integration stage may lead to a political in-fighting between management and labour unions, resulting in a lower performance during the integration stage. Besides, M&As are motivated by the prospect of increasing profit, so a reduction of labour unions' costs could be a source of potential profits (Armah & Peoples, 1997; Heywood & Peoples, 1994), particularly in the case of an unprofitable firm (John et al., 2015), but at the same time, this objective may be a source of conflicts between the managers and the labour unions, which hinder the M&A performance. Moreover, an M&A may create an opportunity to decrease the union density of the firm (Armah & Peoples, 1997). In this scenario, the labour union view the M&A as a threat to the collective agreements (Fallick & Hassett, 1996), so layoffs of unionized workers may not be smooth during the integration (Zeller, 2000), which negatively influence the M&A performance. Worse than that, an M&A can even lead to the removal of the obligation to the labour unions, in case the labour unions do not represent anymore the majority of the workers after the deal (Armah & Peoples, 1997; Heywood & Peoples, 1994). This ‘existing threat’ for the labour union, may result in political in-fighting during the integration stage, resulting in a lower M&A performance.

Nevertheless, if the labour union has strong bargaining power, then it’s likely influenced the restructuring during the integration stage, with less ability to reduce unionized jobs (John et al., 2015) due to the ability of the labour union to resist the planning of the management to cut jobs. Because of this argument, the M&A literature put emphasis on the power of the labour unions in relation to M&A success (Armah & Peoples, 1997; Fallick & Hassett, 1996; Heywood & Peoples, 1994; Rosett, 1990) due to the ability of the labour union to change the nature of the integration, and instead to eliminate duplicate jobs, the management may not remove redundancies as needed in the integration, to avoid industrial relations disputes with a powerful labour union. Given these arguments, the following hypothesis has been developed:

Buyer’s Union versus Seller’s union. The existing literature does not provide theoretical explanations or suggestions for the comparison between the buyer’s union versus the seller’s union in relation to M&A performances. From the standpoint of this study, this limitation allows only to suggest a ground-breaking hypothesis regarding this comparison. Hence, this study assumes that the buyer’s union has more power compared to the seller’s union, because usually the workforce of the buyer is bigger than the workforce of the seller (Rozen-Bakher, 2017a), and as a result, the buyer’s union has more influence on the decisions during the integration. However, regardless of the size of the workforce, the seller’s union can create ‘noises’ during the integration stage through slowdowns and strikes, which may deter the management to cut the power of the seller’s union (Adams & Neely, 2000). Nevertheless, a big seller’s union has more power to change the nature of the integration by resisting cutting jobs during the integration stage. Considering these arguments, the following hypothesis has been developed:

Two Labour Unions (buyer and seller) versus One Labour Union (buyer or seller). The M&A literature nor the labour union literature, do not provide any rationalisations for the pioneering comparison of this study, between a case of an M&A with two labour unions (buyer and seller) versus a case of an M&A with one labour union (buyer or seller). Therefore, this study developed the hypothesis of this comparison based on the Game theory (Osborne, 2004; Camerer, 2011), and in particular, on the differences between Cooperative and Non-cooperative Games (Branzei et al., 2008; Camerer, 2011; Eisenstadt & Moshaiov, 2018; Osborne, 2004). According to the Game theory, in a cooperative game, the players can communicate with each other, and therefore get joint decisions (Branzei et al., 2008; Camerer, 2011; Osborne, 2004). More important, in a cooperative game, the players can coordinate their moves in a binding manner, so that no players will deviate from the method of action that was decided to ensure an effective outcome (Branzei et al., 2008; Camerer, 2011; Osborne, 2004). On the contrary, in a non-cooperative game, the players do not communicate with each other due to a conflict, and as a result, the players need to deal with a lack of information about the moves of the other players, and therefore they cannot make joint decisions, which negatively influence the outcome (Eisenstadt & Moshaiov, 2018; Camerer, 2011; Osborne, 2004).

Considering the above, M&A with two labour unions is more likely to lead to a non-cooperative game with an option of creating a coalition between two players against the third player, while an M&A with one union is more likely to lead to a cooperative game, as shown in Figure 2. Therefore, in the case of an M&A with one labour union, can arise two scenarios – powerful labour union versus powerful management. In both these scenarios, the weak player is less being able to challenge the powerful player, so it’s supposed to lead to a smooth integration stage, resulting in higher M&A performance. Nevertheless, an M&A with one labour union can lead to a non-cooperative game, in case of powerful management along with a powerful seller’s union, particularly in case of a big seller, and especially if the management fears that the seller’s union will claim the right to bargain for the non-union workers of the buyer. The merger between ECI and Tadiran is an example of such case when the buyer and the seller had big equal size, so the seller’s union of Tadiran resisted the merger since the announcement of the merger (GLOBES, 1999), which eventually leads to a failure of the merger (Weber, 2013).

However, when an M&A involves two labour unions, then it may lead to political infighting, because each of the players may try to achieve dominance among the three players (the management, the buyer’s union and the seller’s union), or to achieve dominance by creating a coalition with one of the other players against the third player (Kahan & Rapoport, 2014).

In the light of that, four scenarios can arise in the case of M&A with two labour unions, as shown in Figure 2.:

All three players act against each other.

A coalition is being formed between the management and the buyer’s union against the seller’s union.

A coalition is being formed between management and the seller’s union against the buyer’s union.

A coalition is being formed between the buyer’s union and the seller’s union against the management.

All these four scenarios are supposed to end in the failure of the integration stage. More importantly, it’s less likely that an M&A with two labour unions may lead to a cooperative game. Hence, the main difference between an M&A with two labour unions versus an M&A with one labour union lies in the ability to form a coalition between two players against a third player in the case of two labour unions, which creates the conditions for conflicts, resulting in a lower M&A performance. In light of the above, the following hypothesis has been developed:

Hypothesis 3: M&As with two labour unions (buyer and seller) have a more negative influence on M&A performance at the integration stage compared to M&As with one labour union (buyer or seller).

The Role of the Labour Unions in Different Types of M&A

The type of M&A influences the complexity of the integration, and as a result, it also affects the M&A performance (Calipha et al., 2010; Gugler et al., 2003; Palich et al., 2000; Rozen-Bakher, 2018a). From the standpoint of this study, three types of M&A create more challenges in the implementation of M&A strategy, particularly when a labour union involve in the integration process: cross-border M&A, horizontal M&A and vertical M&A.

Labour Unions in Cross-border M&A. Cross-border M&A refers to an M&A between buyer and seller from different countries (Rozen-Bakher, 2018b; Sarala, 2010; Shimizu et al., 2004). Based on previous studies, the integration in Cross-border M&A is more complicated (Baunsgaard & Clegg, 2013; Chen & Wang, 2014; Child et al., 2001; Kroon et al., 2015; Krug & Nigh, 2001; Mtar, 2010; Shimizu et al., 2004; Rozen-Bakher, 2018d; Very et al., 1996; Weber et al., 2011; Yu et al., 2005) compared to a domestic M&A due to the differences of the location factors [e.g. national culture, (House et al., 2002) and political institutions (Calori et al., 1997)[ between the home country and the host country of the firms (Rozen-Bakher, 2017b), as well as due to the organizational culture differences between the firms that involve in the deal (Rozen-Bakher, 2018b; Shimizu et al., 2004; Weber et al., 2012). The existing literature suggests that conflicts between the management and the workers are likely to increase, when the institutional distance between the two countries is greater (Shimizu et al., 2004), which negatively influence the M&A performance (Hasan et al., 2016), particularly during the integration stage (Rozen-Bakher, 2018d; Weber et al., 2012). This may escalate in the case of different industrial relation systems between the countries of the firms, which reflect through the behaviour of the labour unions involved in the deal. In the light of that, previous studies emphasize the impact of the national industrial relations on the power and behaviour of the labour unions within the country (Cook, 1998; Freeman & Pelletier, 1990; Hean, 2018; Julián, 2018; Preminger, 2018), and even how it influences the decision of the buyer if to buy the seller due to the ‘regime shopping’ (Traxler & Woitech, 2000). For example, the regulation of industrial relations in a specific country may not allow cutting jobs without the approval of the labour union, while in other countries, there are no such limitations.

In general, the existing literature argues that labour unions try to avoid involvement in cross-border M&As (Guillén, 2000; Lommerud et al., 2006) because multinational firms employ practices to reduce the density of the labour unions after the deal (Lawler et al., 2013). Moreover, previous studies argue that a cross-border M&A can have a strong disciplinary effect on the power and the wage demands of the union (Lommerud et al., 2006; Lommerud et al., 2011; Straume, 2003). This may worsen if a full capital flight occurs following a cross-border M&A, which may be harmful to the labour unions and the seller’s workers, especially if all the seller’s jobs are eliminated due to the deal (Lommerud et al., 2011). Considering the arguments outlined above, the following hypotheses have been developed:

Labour Unions in Horizontal M&A. An horizontal M&A involves a combination of buyer and seller that compete in the same market (Rozen-Bakher, 2018a; Tremblay & Tremblay, 2012). Therefore, the integration stage is supposed to be less complicated in a horizontal M&A than in unrelated M&As due to the similarity of operations and activities of the rival firms (Rozen-Bakher, 2018a). Considering that, the M&A literature suggests that horizontal M&As/related M&As positively influence the profit due to the increase of the market power (Homberg et al., 2009; Rozen-Bakher, 2018a; Tremblay & Tremblay, 2012). This is based on the reasoning that related M&A change the market structure, so monopolistic industries may be able to pass higher union costs on their consumers (Heywood & Peoples, 1994), resulting in a higher profit. More importantly, previous studies indicate that horizontal M&As/related M&As increase the performance of M&A due to reducing costs, because of the ability to consolidate more duplicate jobs (Conyon et al., 2002; O'Shaughnessy & Flanagan, 1998) operations and activities in the integration stage compared to unrelated M&As (Haspeslagh & Jemison, 1991; Healy et al., 1992; Rozen-Bakher, 2018a).

Nevertheless, a horizontal M&A can lead to a mixed effect when involves a labour union in the deal. On the one hand, horizontal M&As occurred between rivals to reduce competition, so it strengthens the power of the labour unions, but on the other, it may lower the M&A performance due to the resistance of the labour union to reduce jobs (Rozen-Bakher, 2018a). Green and Cromley (1982) found that in every industry and region in the United States, employment increased immediately following a horizontal M&A. This occurred despite the nature of the integration to remove redundancies by eliminating duplicate jobs and operations (Rozen-Bakher, 2018c). Given the arguments outlined above, the following hypotheses have been developed:

Labour Unions in Vertical M&A. A Vertical M&A involves buyer and seller that have a buyer-seller relationship with two forms of relationship (Rozen-Bakher, 2018a; Tremblay & Tremblay, 2012): The first one is an upstream (backward) vertical that occurs when a manufacturing buyer buys one of its input suppliers (Belderbos et al., 2001). The second one is a downstream (forward) vertical that happens when a firm buys another firm that purchases its product (Guan & Rehme, 2012). However, vertical M&As are much rare compared to the other types of M&As, because only a few firms can be fit for vertical relationships (Meador et al., 1996; Rozen-Bakher, 2018a). Besides, the integration in vertical M&As is more complicated than in horizontal M&As due to the buyer-seller relationship (Rozen-Bakher, 2018a; Tremblay & Tremblay, 2012). This may be due to the need to synchronize the production flow or services between the combined firms, which limits the efficiency gains (Rozen-Bakher, 2018a). Previous studies show a mixed effect in relation to M&A performance. Some studies show that vertical M&As negatively affect the M&A performance during the integration stage (Rozen-Bakher, 2018a; Tremblay & Tremblay, 2012), particularly in relation to the profit due to the failure of creating differential advantages (Bhuyan, 2002). However, other studies found a positive impact on M&A success (Goold & Campbell, 1998; Spiller, 1985), particularly when a vertical M&A undertakes in imperfectly competitive markets (Kedia et al. 2011).

The M&A literature lacks studies that examine the role of a labour union in vertical M&As. Nevertheless, the study of Zhao (2001) gives suggestions for the relationship between labour unions in vertical M&As and M&A performance. This study shows that labour unions in vertical integration lead to an increase in both, union employment and wages, but at the same time, it reduces the profits (Zhao, 2001). This signal the power of the labour unions in vertical M&As, which reflects by the ability of the labour unions to resist cutting jobs during the integration, and even to raise wages, resulting in a lower M&A performance. In light of the arguments presented above, the following hypotheses have been developed:

Considering the arguments presented in the whole this section, the following mediation hypothesis has been formulated:

Hypothesis 6: labour unions mediate the relationship between the types of M&As (cross-border, horizontal and vertical) and M&A performance during the integration stage.

Methodology

Sample and Data Sources

The sample of the study includes only public firms (197 buyers and 197 sellers) that have traded on the stock exchange of the Nasdaq Stock Market (NASDAQ), as well as on the stock exchange of the New York Stock Exchange (NYSE) (NASDAQ, 2018; NYSE, 2018). All the public firms included in the sample were involved in M&A deals. The sample includes firms from many countries worldwide, such as United States, United Kingdom, Australia, Belgium, Canada, Germany, Italy, Switzerland and more. Besides, the sample includes public firms from the three main sectors: agriculture, industry and services.

The database of the study is based on 591 annual reports (10-K) (Rozen-Bakher, 2017a; SEC, 2009) of the public firms that included in the sample, from the years that the M&As took place. Public firms worldwide that have traded on the stock exchanges in the USA, must publish to the public the annual reports (10-K), accordingly to the request of the U.S. Securities and Exchange Commission (SEC) (Rozen-Bakher, 2018c; SEC 2009). Therefore, the public has free access to these annual reports usually publish on the websites of public firms.

Research Method

Evaluation - Accounting Method. The M&A literature presents three approaches for evaluation of M&A performance at the firm level (Rozen-Bakher, 2018a): the event study method (Changjun & Qiaoyue, 2014; Oler et al., 2008), the accounting method (Changjun & Qiaoyue, 2014; Rozen-Bakher, 2018c), and the respondents’ self-estimated rating method (Ahammad et al., 2012; Angwin & Savill, 1997; Trąpczyński et al., 2018; Weber et al., 2011; Zaks et al., 2018).

The current study used the accounting method by analysing the annual reports (10-K) of the public firms. This method is considered the preferred method for assessing M&A performance (McNabb & Whitfield, 1997; Rozen-Bakher, 2017a), because it relies on the ‘hard data’ of the public firms, rather than on the perception of the managers, as done in the respondents’ self-estimated rating method (Huber & Power, 1985; McNabb & Whitfield, 1997; Weber et al. 2011), or based on the present value of future streams of income, as done in the event study method (Rozen-Bakher, 2018a). In other words, there is a big difference between studies that ask the managers to rank the M&A performance based on the manager’s biased opinion (Trąpczyński et al., 2018; Zaks et al., 2018) versus studies that rely on the financial statements of the firm (Rozen-Bakher, 2018a) (for comparison between these three methods, see e.g. Changjun & Qiaoyue, 2014; McNabb & Whitfield, 1997; Rozen-Bakher, 2017a). Hence, this study relied on the financial statements published in the annual reports (10-K) of the public firms included in the sample.

Time Series Analysis. The current study used time-series analyses to examine the changes in the M&A performance between the pre-M&A period and the integration period (Rozen-Bakher, 2018d). The data of the pre-M&A stage is based on the sum of the performances of the buyer and the seller before the M&A took place (Kubo & Saito, 2012; Rozen-Bakher, 2018b), and is collected from the last annual reports of the buyer and the seller before the M&A took place (Rozen-Bakher, 2018a). The data of the integration stage are based on the first buyer's annual report after the M&A took place (Rozen-Bakher, 2018d).

Measures

Mediator variables. The study includes five mediator variables to examine the impact of the labour unions on M&A performance during the integration stage. These variables are defined as dummy variables and are based on the status of the labour unions before the M&A took place (Rozen-Bakher, 2018a).

M&As without Unions. An M&A without labour unions in both the buyer and the seller refers to 1, while others refer to 0.

Buyer’s Union. A labour union of the buyer refers to 1, while others refer to 0.

Seller’s Union. A labour union of the seller refers to 1, while others refer to 0.

M&As with One Union −Buyer or Seller. An M&A with a labour union in only one of the firms, either the buyer or the seller, refers to 1, while others refer to 0.

M&As with Two Unions − Buyer and Seller. An M&A with two labour unions in both the buyer and the seller refers to 1, while others refer to 0.

Dependent variables. The study includes two dependent variables to examine M&A performance.

The volume of Activity, Pre-M&A Stage to Integration Stage. The volume of activity was examined by calculating the change in the revenue (in millions of US$) between the pre-M&A stage and the integration stage (Rozen-Bakher, 2018d).

Profitability, Pre-M&A Stage to Integration Stage. The profitability was examined by calculating the change in the net profit (in millions of US$) between the pre-M&A stage and the integration stage (Rozen-Bakher, 2018d).

Independent variables. The study includes three independent variables to examine the types of M&A. These variables are based on the status of the buyer and the seller in the pre-M&A stage and are defined as dummy variables in this study (Rozen-Bakher, 2018a).

Cross-Border M&As. Cross-border M&As refer to 1, while domestic M&As refer to 0 (Rozen-Bakher, 2018b).

Horizontal M&As. Horizontal M&As refer to 1, while others refer to 0 (Rozen-Bakher, 2018a). Horizontal M&As are measured by the industries' similarities of the buyer and the seller, based on the two-digit level of the International Standard Industrial Classification (ISIC) classification of the United Nations industry classification system (Rozen-Bakher, 2018a; UNSD, 2018).

Vertical M&As. Vertical M&As refer to 1, while others refer to 0. Vertical M&As are measured by the industries' similarities of the buyer and the seller, based on the one-digit level of ISIC (Rozen-Bakher, 2018a; UNSD, 2018).

Control variables. The current study includes three control variables to examine the ratio between the buyer and the seller (Hagedoorn & Duysters, 2002; Kemal, 2011; Rozen-Bakher, 2017a). The ratio of the study refers to the pre-M&A stage (Rozen-Bakher, 2018c).

Revenue Ratio. This variable is examined by using the ratio of the revenue (in millions of US$) of the buyer and the seller in the pre-M&A stage (Rozen-Bakher, 2017a). The revenue ratio signals the similarity of the firm size between the buyer and the seller (Rozen-Bakher, 2018a).

Profitability Ratio. This variable is examined by using the ratio of the net profit (in millions of US$) of the buyer and the seller in the pre-M&A stage (Rozen-Bakher, 2017a).

Labour Productivity Ratio. Labour productivity indicates the efficiency of the labour force in creating the output of the firm (Datta et al., 2005; Rozen-Bakher, 2017a). This variable is examined by using the ratio of the revenue per employee (in millions of US$) of the buyer and the seller in the pre-M&A stage (Rozen-Bakher, 2018c), based on the index ‘revenue per employees’ (Datta et al., 2005; Guthrie, 2001; Rozen-Bakher, 2017a).

Test Analysis

The test analysis of the study is based on a test of a mediation model to examine the hypotheses of the study. The current study used the method of James and Brett (1984) to test the mediation model of the study (Frazier et al., 2004; Rozen Bakher, 2017b; Weber et al., 2011). The existing literature presents several methods for testing a mediation model (Baron & Kenny, 1986; Cohen et al., 2003; Frazier et al., 2004; Wood et al., 2008), and despite the criticism regarding the method of James and Brett (Frazier et al., 2004; Wood et al., 2008), most of the previous studies used this method (Frazier et al., 2004) [For example, international business and M&A studies that used the method of James and Brett: e.g. (Rozen Bakher, 2017b, 2018c; Weber et al., 2011)]. Besides, the study includes testing a variance inflation factor (VIF). This test identifies multicollinearity problems (Chatterjee & Price, 1991; Mansfield & Helms, 1982; Rozen Bakher, 2018b).

Results

Table 1 shows the mean and descriptive statistics of the research variables. Table 2 shows the correlation matrix of the research variables. The correlation matrix shows the results of Path b of the research model, which supports hypothesis H3, but do not support hypotheses H1 and H2. The results of hypothesis H3 show, that M&As with two labour unions are significantly and negatively associated with the M&A performance (only revenue) during the integration process, while M&As with one union show significantly and positively associated with the M&A performance.

Table 3 shows the significant results of Path a. The results do not support hypotheses H4.1, H4.2 and H4.3. Unexpectedly, the results show, that M&As without labour unions are significantly and negatively associated with cross-border M&As, while the buyer’s union and M&As with one labour union are significantly and positively associated with cross-border M&As. However, horizontal and vertical M&As show no significant results regarding all the variables of the labour unions.

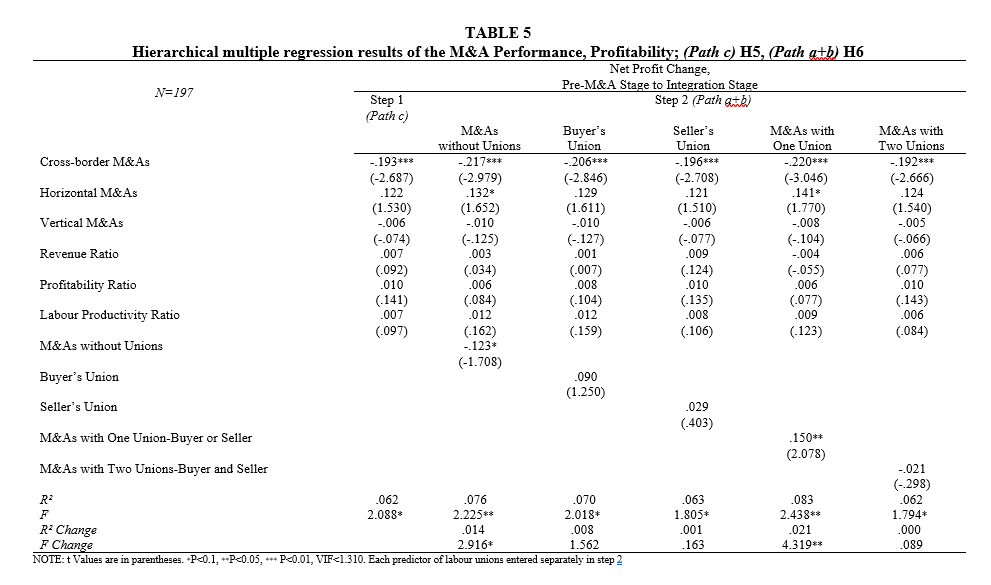

Table 4 and Table 5 show the results of the hierarchical multiple regressions of the mediation research model of the study. Step 1 shows the results of testing Path c of the research model. The results partly support hypotheses H5.1 and H5.3 but do not support H5.2. On the one hand, the results show, as expectedly, that cross-border M&A is significantly and negatively associated with profitability, but on the other, unexpected, cross-border M&A is significantly and positively associated with the volume of activity (revenue). However, the results of the vertical M&A show, as expectedly, that vertical M&A is significantly and negatively associated with the volume of activity (revenue), but without a significant result with the profitability. Even the results of horizontal M&A don’t show significant results in relation to the two variables of M&A performance.

Step 2 shows the results of testing Paths a+b of the research model. The results partially support hypothesis H6. The results show that the buyer’s union, M&As with one labour union and M&As with two labour unions mediate the relationship between the types of M&A and the volume of activity (revenue) during the integration stage. However, the results show that M&As without labour unions and M&As with one labour union mediate the relationship between the types of M&A and profitability during the integration stage. Nevertheless, the seller’s union does not mediate the relationship between the types of M&A in relation to the two variables of M&A performance. More importantly, on the one hand, the results show, that M&As with one labour union positively influence the volume of activity (revenue) and the profitability, but on the other, the buyer’s union and the M&As with two labour unions negatively influence the volume of activity (revenue), while only M&As without labour unions negatively influence the profitability.

Discussion

The analysis of the study highlights the originality of this research, which is reflected in an innovative comparison between the multiple variables of the labour unions presented in this study, as shown in Figure 3 which presents the summary of the significant results of this study. Analysing the results confirms the justify of exploring this phenomenon through a mediation research model. More specifically, analysing the results of the correlation matrix along with the hierarchical multiple regression, reveals that the correlation matrix does not show significant results between all the labour unions variables and profitability. However, the hierarchical multiple regressions that test the labour unions as a mediator variable between the types of M&A and M&A performance reveal significant results between some of the labour unions variables and profitability. In other words, direct relationships between all the variables of labour unions and profitability do not show significant correlations, while indirect relationships through the mediating model show significant results. This meant that the type of M&A has a significant role in explaining the M&A performance (Rozen-Bakher, 2018a), as shown in this study, particularly when the type of M&A is used as an antecedent variable in a mediation research model (Rozen-Bakher, 2018c). That revelation highpoint the importance of using a mediating research model in M&A studies (Rozen-Bakher, 2018c; Weber et al., 2011).

Moreover, the study reveals the importance of using the Game theory to explain the differences between an M&A with one labour union and an M&A with two labour unions, through the differences between cooperative and non-cooperative games (Branzei et al., 2008; Eisenstadt & Moshaiov, 2018; Osborne, 2004). The study suggests that an M&A with two labour unions complicated the integration process due to the conflicts that arise between the players (management, buyer’s union, seller’s union), because of the coalition that formed between two players against a third player (as presented in Figure 2), which hinder the M&A performance. However, the study suggests that an M&A with one labour union is less motivated to form a coalition, because exist only two players, so it’s less likely that the players get into a non-cooperative game. This decreases the conflicts between the two players during the integration, resulting in higher M&A performance. More importantly, the study reveals that an M&A with one labour union leads to a ‘win-win scenario’ (Rozen-Bakher, 2018c), which reflects in higher profitability (net profit) along with a higher volume of activity (revenue).

Furthermore, the study reveals a surprising result in relation to M&As without labour unions. The results show that M&As without labour unions negatively influence profitability. This confirms the argument that the power of the labour union can contribute to the profitability of the firm. Besides, the analysis of the study reveals a complex mixed effect in cross-border M&As. On the one hand, a cross-border M&A leads to higher revenue, but at the same time, to lower profitability. On the other hand, a cross-border M&A empower the buyer’s union. This suggests that in cross-border M&As, the buyer has more influence on the integration decisions compared to the seller. More cross-border M&As studies are needed in the future to investigate this phenomenon.

Conclusions

Due to the high failure rate of M&A strategy (King et al., 2004; Kumar & Sharma, 2019; Matsumoto, 2019; Renneboog & Vansteenkiste, 2019; Rozen-Bakher, 2018c; Sarala, 2010; Steger & Kummer, 2007; Tichy, 2001; Venema, 2015; Thelisson, 2020; Weber et al., 2012), this study raises the question of how the labour unions affect the M&A performance during the integration process. The study used the Game Theory to explain the non-cooperative games that arise between the players (management, buyer’s union and seller’s union) during the integration stage, particularly in relation to the difference between an M&A with one labour union (cooperative game) and an M&A with two labour union (non-cooperative game).

The integration stage is considered as the ‘weakest link’ in the M&A strategy (Rozen-Bakher, 2018d), and the most problematic stage in the M&A process (Baunsgaard & Clegg, 2013; Chen & Wang, 2014; Mtar, 2010; Rozen-Bakher, 2018b; Shimizu et al., 2004; Very et al., 1996; Yu et al., 2005), because it leads to organizational change and jobs cutting due to the nature of the integration stage (Deakin & Slinger, 1997; Gibbs, 1993; Haspeslagh & Jemison, 1991; Lehto & Böckerman, 2008; O’Shaughnessy & Flanagan, 1998; Rozen-Bakher, 2018c). The integration process may be more complicated if a labour union is involved in the deal and actively resist the reduction of jobs during the integration, resulting in a negatively influence on the M&A performance (Hirsch, 1991). However, the complication of the integration may be worsened when an M&A involves two labour unions, which may lead to political infighting, because each of the players may try to achieve dominance among the three players (the management, the buyer’s union and the seller’s union), or to achieve dominance by creating a coalition with one of the other players against the third player (Kahan & Rapoport, 2014).

In the light of the above, the study presents a novel set of labour unions variables: M&As without labour unions, buyer’s union, seller’s union, M&As with one union (buyer or seller) and M&As with two unions (buyer and seller). The study used the accounting method to evaluate the M&A performance by analysing 591 annual reports (10-K) of public firms that have traded on NASDAQ and NYSE

These results highlight the importance of using the Game theory (Branzei et al., 2008; Eisenstadt & Moshaiov, 2018; Osborne, 2004) aimed to explain the difference between an M&A with one labour union (cooperative game) and an M&A with two labour union (non-cooperative game). The study demonstrates that an M&A with two labour union leads to the worst scenario – ‘lose-lose scenario’ (Rozen-Bakher, 2018c) that reflect in a negative influence on both the revenue and the profitability. This suggests that an M&A with two labour union leads to conflicts during the integration stage due to the ability to form a coalition between two players against a third player, which hinder the M&A performance. On the contrary, the study reveals that an M&A with one labour union leads to a ‘win-win scenario’ (Rozen-Bakher, 2018c) that reflect a positive influence on both the revenue and profitability of the M&A. This suggests that the existence of only two players leads to a pointless to form a coalition, which decreases the conflicts between the two players (management and labour union-buyer or seller), resulting in higher M&A performance.

The study presents two fundamental implications for managers: First, the study emphasizes the need to avoid M&As with two labour unions due to the high probability of failure in this kind of M&A. Nonetheless, management that decides to take the challenge, and to deal with an M&A with two labour unions, should prepare for decreasing the conflicts with the labour unions, and more importantly, to avoid the temptation of forming a coalition with one of the labour unions against the third one. Only strategy of a cooperative game with sophisticated tactics to establish a cooperative game (Branzei et al., 2008; Osborne, 2004), despite that the nature situation is a non-cooperative game, may be able to succeed this problematic M&A with two labour unions. Second, many managers oppose business with labour unions due to the common argument that the labour unions hinder the success of the firm. This comes to forth, particularly in M&As, due to the high failure rate of M&A strategy, regardless of the involvement of labour unions in the deal. However, despite the outlined above, managers should favourite an M&A with one labour union, particularly when the seller has a labour union, especially if the seller is smaller relative to the buyer, because it may lead to a rare scenario in the M&A strategy, to a ‘win-win scenario’ (Rozen-Bakher, 2018c) that reflect in a higher revenue with higher profitability. The study concludes that an M&A with two labour unions (buyer and seller) has a high risk for failure, while an M&A with one labour union (buyer or seller) creates opportunities for success.

Limitations of the Study and Future Research

The limitation of the study is mainly due to the lack of previous studies, especially new ones, that explore the relationship between the labour unions and M&A performance. This limitation compelled the development of the theoretical background of the study on relatively old studies due to the lack of new studies on that topic. Therefore, this study highlights the need for new studies on that topic to develop a well-grounded theoretical foundation regarding the role of labour unions in M&As. More importantly, this study raises the need for future studies that will examine additional antecedent factors in relation to the role of labour unions in the M&A activity (Bauer & Matzler, 2014). Future research should also explore the impact of labour unions on M&A performance by using different research methods (Cartwright et al., 2012). Finally, emphasis should be given for future studies that will explore in-depth how the labour unions influence the M&A performance in cross-border M&As.

References

Adams, C., & Neely, A. (2000). The performance prism to boost M&A success. Measuring business excellence, 4(3), 19-23.

Ahammad, M. F., Glaister, K. W., Weber, Y., & Tarba, S. Y. (2012). Top management retention in cross-border acquisitions: the roles of financial incentives, buyer’s commitment and autonomy. European Journal of International Management, 6(4), 458-480.

Angwin, D., & Savill, B. (1997). Strategic perspectives on European cross-border acquisitions: A view from top European executives. European Management Journal, 15(4), 423-435.

Armah, B., & Peoples, J. (1997). Foreign Corporate Acquisition Activity Domestic Union Status in the US. International Economic Journal, 11(3), 103-115.

Baron, R. M., & Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173.

Bauer, F., & Matzler, K. (2014). Antecedents of M&A success: The role of strategic complementarity, cultural fit, and degree and speed of integration. Strategic management journal, 35(2), 269-291.

Baunsgaard, V. V., & Clegg, S. (2013). ‘Walls or boxes’: The effects of professional identity, power and rationality on strategies for cross-functional integration. Organization Studies, 34(9), 1299-1325.

Becker, B. E., & Olson, C. A. (1989). Unionization and shareholder interests. ILR Review, 42(2), 246-261.

Belderbos, R., Capannelli, G., & Fukao, K. (2001). Backward vertical linkages of foreign manufacturing affiliates: Evidence from Japanese multinationals. World development, 29(1), 189-208.

Bhuyan, S. (2002). Impact of vertical mergers on industry profitability: an empirical evaluation. Review of Industrial Organization, 20(1), 61-79.

Branzei, R., Dimitrov, D., & Tijs, S. (2008). Models in cooperative game theory (Vol. 556). Springer Science & Business Media.

Calipha, R., Tarba, S., & Brock, D. (2010). Mergers and acquisitions: a review of phases, motives, and success factors. Advances in Mergers and Acquisitions, 9(1), 1-24.

Calori, R., Lubatkin, M., Very, P., & Veiga, J. F. (1997). Modelling the origins of nationally-bound administrative heritages: A historical institutional analysis of French and British firms. Organization Science, 8(6), 681-696.

Camerer, C. F. (2011). Behavioral game theory: Experiments in strategic interaction. Princeton University Press.

Cartwright, S., Teerikangas, S., Rouzies, A., & Wilson-Evered, E. (2012). Methods in M&A—A look at the past and the future to forge a path forward. Scandinavian Journal of Management, 28(2), 95-106.

Changjun, Y., & Qiaoyue, L. (2014). The study of the performance of manufacturing enterprises cross-border M&A in China based on super-efficiency DEA. Journal of Chemical and Pharmaceutical Research, 6, 1942-1945.

Chatterjee, S. & Price, B. (1991). Regression diagnostics. New York.

Chen, H. J., Kacperczyk, M., & Ortiz-Molina, H. (2011). Labor unions, operating flexibility, and the cost of equity. Journal of Financial and Quantitative Analysis, 46(1), 25-58.

Chen, H. J., Kacperczyk, M., & Ortiz-Molina, H. (2012). Do nonfinancial stakeholders affect the pricing of risky debt? Evidence from unionized workers. Review of Finance, 16(2), 347-383.

Chen, F., & Wang, Y. (2014). Integration risk in cross-border M&A based on internal and external resource: empirical evidence from China. Quality & Quantity, 48(1), 281-295.

Child, J., Faulkner, D., & Pitkethly, R. (2001). The Management of International Acquisitions. Oxford University Press.

Cohen, J., Cohen, P., West, S. G., & Aiken, L. S. (2013). Applied multiple regression/correlation analysis for the behavioral sciences. Routledge.

Cook, M.L. (1998). Toward flexible industrial relations? Neo-liberalism, democracy, and labor reform in Latin America. Industrial Relations, 37(3): 311-336.

Conyon, M. J., Girma, S., Thompson, S., & Wright, P. W. (2002). The impact of mergers and acquisitions on company employment in the United Kingdom. European Economic Review, 46(1), 31-49.

Datta, D. K., Guthrie, J. P., & Wright, P. M. (2005). Human resource management and labor productivity: does industry matter?. Academy of Management Journal, 48(1), 135-145.

Davidsson, J. B., & Emmenegger, P. (2013). Defending the organisation, not the members: Unions and the reform of job security legislation in Western Europe. European Journal of Political Research, 52(3), 339-363.

Deakin, S., & Slinger, G. (1997). Hostile takeovers, corporate law, and the theory of the firm. Journal of Law and Society, 24(1), 124-151.

Declerck, F. (2003). Valuation of seller firms acquired in the food sector during the 1996-2001 wave. International Food and Agribusiness Management Review, 5(4), 1-16.

Doucouliagos, H., & Laroche, P. (2009). Unions and Profits: A Meta‐Regression Analysis1. Industrial Relations: A Journal of Economy and Society, 48(1), 146-184.

Eisenstadt, E., & Moshaiov, A. (2018). Decision‐making in non‐cooperative games with conflicting self‐objectives. Journal of Multi‐Criteria Decision Analysis. DOI: doi.org/10.1002/mcda.1639

Fallick, B. C., & Hassett, K. A. (1996). Unionization and acquisitions. Journal of Business, 51-73.

Frazier, P. A., Tix, A. P., & Barron, K. E. (2004). Testing moderator and mediator effects in counseling psychology research. Journal of Counseling Psychology, 51(1), 115.

Freeman, R., & Pelletier, J. (1990). The Impact of Industrial Relation Legislation on British Union Density. British J. of Industrial Relations, 28(2), 141-162.

Gates, S., & Very, P. (2003). Measuring performance during M&A integration. Long Range Planning, 36(2), 167-185.

Gibbs, P. A. (1993). Determinants of corporate restructuring: the relative importance of corporate governance, takeover threat and free cash flow. Strategic Management Journal, 14, 51–68.

GLOBES. (1999). Tadiran-ECI: A merger with a problem. GLOBES, 04.01.1999. https://www.globes.co.il/news/article.aspx?did=101176

Golden, M. A. (1997). Heroic Defeats.The Politics of Job Loss. UK: Cambridge University Press.

Goold, M., & Campbell, A. (1998). Desperately seeking synergy. Harvard Business Review, 76, 131-143.

Guan, W., & Rehme, J. (2012). Vertical integration in supply chains: driving forces and consequences for a manufacturer's downstream integration. Supply Chain Management: An International Journal, 17(2), 187-201.

Gugler, K., Mueller, D. C., Yurtoglu, B. B., & Zulehner, C. (2003). The effects of mergers: an international comparison. International Journal of Industrial Organization, 21(5), 625-653.

Guillén, M. F. (2000). Organized labor's images of multinational enterprise: Divergent foreign investment ideologies in Argentina, South Korea, and Spain. ILR Review, 53(3), 419-442.

Guthrie, J. P. (2001). High-involvement work practices, turnover, and productivity: Evidence from New Zealand. Academy of Management Journal, 44, 180-190.

Green, B. M. & Cromley, G. R. (1982). The Horizontal Merger: its Motives and Spatial Employment Impacts. Economic Geography, 58, 358-370

Hagedoorn, J., & Duysters, G. (2002). The effect of mergers and acquisitions on the technological performance of companies in a high-tech environment. Technology Analysis & Strategic Management, 14(1), 67-85.

Hasan, M. M., Ibrahim, Y., & Uddin, M. M. (2016). Institutional distance factors influencing firm performance: A hypothetical framework from cross-border mergers and acquisitions. The Journal of Developing Areas, 50(6), 377-386.

Haspeslagh, P. C., & Jemison, D. B. (1991). Managing Acquisitions: Creating Value Through Corporate Renewal (Vol. 416). New York: Free Press.

Healy, P. M., Palepu, K. G., & Ruback, R. S. (1992). Does corporate performance improve after mergers?. Journal of Financial Economics, 31(2), 135-175.

Hean, L. O. (2018). Industrial Relations in Singapore: Practice and Perspective. World Scientific.

Heywood, J. S., & Peoples, J. H. (1994). Unions and the pattern of corporate mergers: US evidence. Labour Economics, 1(2), 203-221.

Hirsch, B. T. (1991). Union coverage and profitability among US firms. The Review of Economics and Statistics, 69-77.

Homberg, F., Rost, K., & Osterloh, M. (2009). Do synergies exist in related acquisitions? A meta-analysis of acquisition studies. Review of Managerial Science, 3(2), 75-116.

House, R., Javidan, M., Hanges, P., & Dorfman, P. (2002). Understanding cultures and implicit leadership theories across the globe: an introduction to project GLOBE. Journal of World Business, 37(1), 3-10.

Huber, G. P., & Power, D. J. (1985). Retrospective reports of strategic‐level managers: Guidelines for increasing their accuracy. Strategic Management Journal, 6(2), 171-180.

James, L. R., & Brett, J. M. (1984). Mediators, moderators, and tests for mediation. Journal of Applied Psychology, 69(2), 307.

John, K., Knyazeva, A., & Knyazeva, D. (2015). Employee rights and acquisitions. Journal of Financial Economics, 118, 49-69.

Julián, D. (2018). Unions Opposing Labor Precarity in Chile: Union Leaders’ Perceptions and Representations of Collective Action. Latin American Perspectives, 45(1), 63-76.

Kahan, J. P., & Rapoport, A. (2014). Theories of coalition formation. Psychology Press.

Kedia, S., Ravid, S. A., & Pons, V. (2011). When do vertical mergers create value?. Financial Management, 40(4), 845-877.

Kemal, M. U. (2011). Post-merger profitability: A case of Royal Bank of Scotland (RBS). International Journal of Business and Social Science, 2(5), 157-162.

King, D. R., Dalton, D. R., Daily, C. M., & Covin, J. G. (2004). Meta‐analyses of post‐acquisition performance: Indications of unidentified moderators. Strategic Management Journal, 25(2), 187-200.

Krishnan, H. A., & Park, D. (2002). The impact of work force reduction on subsequent performance in major mergers and acquisitions: an exploratory study. Journal of Business Research, 55(4), 285-292.

Krishnan, H. A., Hitt, M. A., & Park, D. (2007). Acquisition premiums, subsequent workforce reductions and post‐acquisition performance. Journal of Management Studies, 44(5), 709-732.

Kroon, D. P., Cornelissen, J. P., & Vaara, E. (2015). Explaining employees’ reactions towards a cross-border merger: the role of English language fluency. Management International Review, 55(6), 775-800.

Krug, J.A., & Nigh, D. (2001) Executive perceptions in foreign and domestic acquisitions: An analysis of foreign ownership and its effect on executive fate. Journal of World Business,36(1), 85-105.

Kubo, K., & Saito, T. (2012). The effect of mergers on employment and wages: Evidence from Japan. Journal of The Japanese and International Economies, 26, 263-284.

Kumar, V., & Sharma, P. (2019). Why Mergers and Acquisitions Fail?. In An Insight into Mergers and Acquisitions (pp. 183-195). Palgrave Macmillan, Singapore.

Laroche, P., & Wechtler, H. (2011). The effects of labor unions on workplace performance: New evidence from France. Journal of Labor Research, 32(2), 157-180.

Lawler, J. J., Chang, P. C., Hong, W., Chen, S. J., Wu, P. C., & Bae, J. (2013). Going abroad: HR policies, national IR systems, and union activity in foreign subsidiaries of US multinationals. ILR review, 66(5), 1149-1171.

Lee, D. S., & Mas, A. (2012). Long-run impacts of unions on firms: New evidence from financial markets, 1961–1999. The Quarterly Journal of Economics, 127(1), 333-378.

Lehto, E., & Böckerman, P. (2008). Analysing the employment effects of mergers and acquisitions. Journal of Economic Behavior & Organization, 68(1), 112-124.

Lommerud, K. E., Meland, F., & Straume, O. R. (2011). Mergers and capital flight in unionised oligopolies: Is there scope for a “national champion” policy? International Review of Economics & Finance, 20(2), 325-341.

Lommerud, K. E., Straume, O. R., & Sørgard, L. (2006). National versus international mergers in unionized oligopoly. The Rand Journal of Economics, 37(1), 212-233.

Mansfield, E. R., & Helms, B. P. (1982). Detecting multicollinearity. The American Statistician, 36(3a), 158-160.

Matsumoto, S. (2019). The Causes of Failure: Case Studies of Eight Failed Acquisitions Ending in a Sale or Withdrawal at a Loss. In Japanese Outbound Acquisitions (pp. 65-105). Palgrave Macmillan, Singapore.

Meador, A. L., Church, P. H., & Rayburn, L. G. (1996). Development of prediction models for horizontal and vertical mergers. Journal of financial and strategic decisions, 9(1), 11-23.

McNabb, R., & Whitfield, K. (1997). Unions, flexibility, team working and financial performance. Organization Studies, 18(5), 821-838.

Mtar, M. (2010). Institutional, industry and power effects on integration in cross-border acquisitions. Organization Studies, 31(8), 1099-1127.

NASDAQ, Nasdaq Stock Market. (2018). Nasdaq Stock Market. https://business.nasdaq.com/

NYSE, New York Stock Exchange. (2018). New York Stock Exchangehttps://www.nyse.com/index

Osborne, M.J. (2004). An Introduction to Game Theory. New York: Oxford University Press.

Oler, D. K., Harrison, J. S., & Allen, M. R. (2008). The danger of misinterpreting short-window event study findings in strategic management research: an empirical illustration using horizontal acquisitions. Strategic Organization, 6(2), 151-184.

O'Shaughnessy, K. C., & Flanagan, D.J. (1998). Determinants of layoff announcements following M&As: An empirical investigation. Strategic Management Journal, 19(10), 989-999.

Pablo, A. L. (1994). Determinants of acquisition integration level: A decision-making perspective. Academy of Management Journal, 37(4), 803-836.

Palich, L.E., Cardinal, L.B., & Miller, C.C. (2000). Curvilinearity in the diversification-performance linkage: An examination of over three decades of research. Strategic Management Journal, 21(2), 155-174.

Palokangas, T. (1996). Endogenous growth and collective bargaining. J. of Economic Dynamics and Control, 20, 925-44.

Palokangas, T. (2000). Labor Unions, Public Policy and Economic Growth. United Kingdom: Cambridge University Press.

Preminger, D. J. (2018). Focus: Trade unions in Israel: a resurgence of unionism?. International Union Rights, 25(2), 18-28.

Puranam, P., Singh, H., & Chaudhuri, S. (2009). Integrating acquired capabilities: When structural integration is (un) necessary. Organization Science, 20(2), 313-328.

Reddy, K. S., Nangia, V. K., & Agrawal, R. (2012). Mysterious broken cross-country M&A deal: Bharti Airtel-MTN. Journal of the International Academy for Case Studies, 18(7), 61-75.

Renneboog, L., & Vansteenkiste, C. (2019). Failure and success in mergers and acquisitions. Journal of Corporate Finance, 58, 650-699.

Rosett, J. G. (1990). Do union wealth concessions explain takeover premiums?: The evidence on contract wages. Journal of Financial Economics, 27(1), 263-282.

Rozen-Bakher, Z. (2017a). Labour Productivity in M&As: Industry Sector vs. Services Sector. The Service Industries Journal. DOI: 10.1080/02642069.2017.1397136

Rozen-Bakher, Z. (2017b). Impact of Inward and Outward FDI on Employment: The Role of Strategic Asset-Seeking FDI. Transnational Corporations Review, 9(1), 16-30. DOI: 10.1080/19186444.2017.1290919.

Rozen-Bakher, Z. (2018a). Comparison of Merger and Acquisition (M&A) Success in Horizontal, Vertical and Conglomerate M&As: Industry Sector vs. Services Sector. The Service Industries Journal, 38(7-8), 492-518. DOI: 10.1080/02642069.2017.1405938.

Rozen-Bakher, Z. (2018b). How do each dimension of Hofstede’s national culture separately influence M&A success in cross-border M&As?. Transnational Corporations Review. DOI:10.1080/19186444.2018.1475089

Rozen-Bakher, Z. (2018c). The Trade-off Between Synergy Success and Efficiency Gains in M&A Strategy. EuroMed Journal of Business. DOI: 10.1108/EMJB-07-2017-0026

Rozen-Bakher, Z. (2018d). Could the pre-M&A performances Predict Integration Risk in Cross-Border M&As? International Journal of Organizational Analysis, 26(4). DOI: 10.1108/IJOA-07-2017-1199.

Sarala, R. M. (2010). The impact of cultural differences and acculturation factors on post-acquisition conflict. Scandinavian Journal of Management, 26(1), 38-56.

SEC, U.S. Securities and Exchange Commission. (2009). U.S. Securities and Exchange Commission. https://www.sec.gov/fast-answers/answers-form10khtm.html , Last modified, June 26, 2009.

Shimizu, K., Hitt, M. A., Vaidyanath, D., & Pisano, V. (2004). Theoretical foundations of cross-border mergers and acquisitions: A review of current research and recommendations for the future. Journal of International Management, 10(3), 307-353.

Spiller, P. T. (1985). On vertical mergers. Journal of Law, Economics, & Organization, 1(2), 285-312.

Stahl, G. K., & Voigt, A. (2008). Do cultural differences matter in mergers and acquisitions? A tentative model and examination. Organization Science, 19(1), 160-176.

Steger, U., & Kummer, C. (2007). Why merger and acquisition (M&A) waves reoccur: the vicious circle from pressure to failure. IMD.

Saavedra-Chanduví, J. & Torero, M. (2002). Union density changes and union effects on firm performance in Peru (No. 3158). Inter-American Development Bank, Research Department.

Straume, O. R. (2003). International mergers and trade liberalisation: implications for unionised labour. International Journal of Industrial Organization, 21(5), 717-735.

Thelisson, A. S. (2020). Managing failure in the merger process: evidence from a case study. Journal of Business Strategy.

Tichy, G. (2001). What do we know about success and failure of mergers? Journal of Industry, Competition and Trade, 1(4), 347-394.

Trąpczyński, P., Zaks, O., & Polowczyk, J. (2018). The Effect of Trust on Acquisition Success: The Case of Israeli Start-Up M&A. Sustainability, 10(7), 1-16.

Traxler, F., & Woitech, B. (2000). Transnational Investment and National Labour Market Regimes: A Case of Regime Shopping'?. European Journal of industrial relations, 6(2), 141-159.

Tremblay, V. J., & Tremblay, C. H. (2012). Horizontal, Vertical, and Conglomerate Mergers. In New Perspectives on Industrial Organization (pp. 521-566). Springer New York.

UNSD, United Nations Statistics Division. (2018). International Standard Industrial Classification of All Economic Activities (ISIC). https://unstats.un.org/unsd/publications/catalogue?selectID=318

Venema, W. H. (2015). Integration: The Critical M&A Success Factor. Journal of Corporate Accounting & Finance, 26(4), 23-27.

Very, P., Lubatkin, M., & Calori, R. (1996). A cross-national assessment of acculturative stress in recent European mergers. International Studies of Management & Organization, 26(1), 59-86.

Weber, Y. (2013). A comprehensive guide to mergers & acquisitions: Managing the critical success factors across every stage of the M&A process. FT Press.

Weber, Y., Tarba, S. Y., & Rozen-Bachar, Z. (2011). Mergers and acquisitions performance paradox: the mediating role of integration approach. European Journal of International Management, 5(4), 373-393.

Weber, Y., Tarba, S. Y., & Rozen-Bachar, Z. (2012). The effects of culture clash on international mergers in the high tech industry. World Review of Entrepreneurship, Management and Sustainable Development, 8(1), 103-118.

Wood, R. E., Goodman, J. S., Beckmann, N., & Cook, A. (2008). Mediation testing in management research a review and proposals. Organizational Research Methods, 11(2), 270-295.

Yu, J., Engleman, R. M., & Van de Ven, A. H. (2005). The integration journey: An attention-based view of the merger and acquisition integration process. Organization Studies, 26(10), 1501-1528.

Zaks, O., Polowczyk, J., & Trąpczyński, P. (2018). Success Factors of Start-Up Acquisitions: Evidence from Israel. Entrepreneurial Business and Economics Review, 6(2), 201-216.

Zeller, C. (2000). Rescaling Power Relations between Trade Unions and Corporate Management in a Globalising Pharmaceutical Industry: The Case of the Acquisition of Boehringer Mannheim by Hoffman—La Roche. Environment and Planning A, 32(9), 1545-1567.

Zhao, L. (2001). Unionization, vertical markets, and the outsourcing of multinationals. Journal of International Economics, 55(1), 187-202.

Zollo, M., & Meier, D. (2008). What is M&A performance?. The Academy of Management Perspectives, 22(3), 55-77.